Stock compensation can be a great pathway to wealth, but they also come with their own set of tax implications. Unfortunately, many taxpayers miss important tax considerations when it comes to stock compensation.

In this post, we will explore the top five things that are often missed when it comes to taxes and stock compensation, including:

- Not reporting capital gains (or losses) on the sale of stock

- Double counting income

- Forgetting about Alternative Minimum Tax on ISOs

- Forgetting about the AMT tax credit

- Large balances due (and interest and penalties) at tax filing time.

If you can avoid even one of these mistakes, you might save $1000s in taxes and fees to a tax advisor to re-do incorrectly done tax returns…not to mention a gigantic hassle.

[Flow’s Note: This post was written by guest blogger John McCarthy. John’s firm, McCarthy Tax Preparation, is a tax preparation and planning firm that has been serving clients since 2001. Their mission is to help technology employees with proactive tax planning for their equity compensation. Learn more about John and his firm, or schedule an introductory call.]

A “Brief” Summary of Stock Compensation Tax Reporting

The surest way to get yourself in hot water with the IRS is to not report stock options correctly on your tax return. Each type of stock compensation is handled differently, so it’s important to know what reporting you are responsible for.

Let’s take a look at the tax treatment at various stages:

| TYPE OF STOCK COMPENSATION | STAGE 1: GRANT (when shares are awarded to you; usually they’re not yours yet) | STAGE 2: VEST | STAGE 3: EXERCISE/PURCHASE | STAGE 4: SALE |

| Employee Stock Purchase Plan (ESPP) | The start of the Offering Period No tax reporting | During the Purchase Period No tax reporting | At the end of the Purchase Period, when shares are automatically purchased for you. No tax reporting | Either Ordinary Income or Capital Gains |

| Restricted Stock Units (RSU) | No tax reporting | When the RSUs turn into shares of stock for you Ordinary Income on your paystub and tax withholding | n/a | Capital Gain or Loss |

| Non-Qualified Stock Options (NQSO) | No tax reporting | When the options vest, you are now permitted, not obligated, to exercise them to own a share of stock No tax reporting | When you pay the strike price to turn the option into a share of stock you own Ordinary Income on your paystub and tax withholding | Capital Gain or Loss |

| Incentive Stock Options (ISO) – Disqualified Disposition (sold before one year of exercise or two years from grant) | No tax reporting | When the options vest, you are now permitted, not obligated, to exercise them to own a share of stock No tax reporting | When you pay the strike price to turn the option into a share of stock you own Ordinary Income on your paystub (no tax withholding) | Capital Gain or Loss |

| Incentive Stock Options (ISO) – Qualified Disposition | No tax reporting | When the options vest, you are now permitted, not obligated, to exercise them to own a share of stock No tax reporting | When you pay the strike price to turn the option into a share of stock you own Possible Alternative Minimum Tax (AMT) | Capital Gain or Loss & AMT Credit |

| Restricted Stock – 83(b) election (explanation below) | Ordinary Income added to your 1040 (i.e., not on your paystub, no tax withholding) | No tax reporting | No tax reporting | Capital Gain or Loss |

As you can see, there are many tax reporting requirements, and reporting can be quite a bit different depending on what type of stock compensation you receive.

In general, the IRS wants their share whenever there has been a transfer of value to you.

At grant and at vesting, there is generally no further action that you need to take on your return, with one exception:

83(b) Election (“Early Exercise”)

If you’ve received Restricted Stock (sometimes called “founder stock”, very low-value stock often given to early employees at a start-up) you may want to consider an 83(b) election. An 83(b) election allows you to report income at a possibly (hopefully) much lower value and starts the clock on lower capital gains rates.

Timing is important here, because the IRS requires this election within 30 days of you receiving this stock. 83(b) elections are outside the scope of this article, so please be sure to see your tax advisor if this applies to you.

Which takes us to the first commonly missed item…

Mistake #1: Not Reporting Capital Gains (or Losses) on the Sale of Stock

As the chart above indicates, you must always report sales when stock is sold.

People often get confused about the taxes and withholding at the vesting or exercise and how that affects the reporting when the shares are sold. Clients often think that because taxes were already withheld, nothing needs to be reported to the IRS on the sale. This results in tons of notices and correspondence from the IRS.

The IRS receives a Form 1099 reporting document from the company (ex. Shareworks, Fidelity, etc) that holds your options. This document reports the total gross proceeds from the sale, but is often missing the value of the stock compensation that was already included in your W2 as income, aka your “cost basis.”

Consequently, the IRS expects to see a large gain reported from the sale, until you tell them otherwise. This is why reporting your stock sales on Schedule D of your return is so critical.

This is where you tell the IRS that you’ve already paid taxes on these options (through payroll tax withholding), by making an adjustment to the cost basis reported on the Schedule D. You are subtracting your cost basis from the sales proceeds, which reduces your taxable gain. This lowers your tax bill.

Speaking of cost basis…

Mistake #2: Double Counting Income

Remember those 1099s we just talked about?

More often than not, they show the incorrect cost basis. If you take this information straight from the 1099 reporting form, you risk paying double the tax on the sale of this kind of stock compensation:

- RSUs

- NSOs, and

- ISO shares that you’ve owned for less than a year

Why can’t we rely on the 1099s issued?

Get this, the IRS prohibits brokers (like Shareworks, Fidelity) from including the compensation income recognized by the employee in the cost basis reported on Form 1099-B.

So the IRS is actively making it more difficult for you to file your tax return. Great. Just Great.

The bit of good news here is that most brokers make it relatively easy to find the information needed to avoid double paying tax on your option sales. Buried somewhere in the tax document section of your portal, you should see a document called “Supplemental Tax Information”. Be sure to download this and include it with your tax documents. Your tax pro is going to need it.

And if you’ve discovered a mistake on a past return, keep in mind you have three years from the due date of the return to file a correction or amended return. We can’t count the number of these we have done for clients in this exact situation.

So…what about ISOs?

Mistake #3: Forgetting about Alternative Minimum Tax on ISOs

In our table above you can see that, in general, any tax consequences at exercise are handled through your company’s payroll. The exception would be Incentive Stock Options.

ISOs will often trigger Alternative Minimum Tax (“AMT”) if you hold your shares for one year after exercise (a qualified disposition).

What is AMT? The Alternative Minimum Tax (AMT) is a separate tax system designed to ensure that people with higher income pay a minimum amount of taxes.

It was originally created to prevent wealthy taxpayers from using deductions and credits to reduce their tax liability to zero. The AMT has a separate set of rules and exemptions, and taxpayers must calculate their liability under both the regular tax system and the AMT to determine which is higher.

One of the big differences between Regular and AMT tax computation is the treatment of ISOs.

When you exercise an ISO, you are deemed to have received value (income) for the difference between the current fair market value (in a private company, this is the 409(a) value) and the strike price (aka, exercise price) of the shares. You have to report this income on Form 6251 for AMT purposes, even though you haven’t sold (or couldn’t sell) the shares from exercising options.

Keep in mind that there is no withholding tax when you exercise ISOs.

You want to be doubly sure of the tax consequences of exercising ISOs before you exercise. We’ve seen clients with six-figure AMT tax bills that are restricted from selling the shares in pre-IPO companies.

So, what happens to all that AMT tax when you sell shares? I’m so glad you asked…

Mistake #4: Forgetting about the AMT Tax Credit

If there’s any good news about paying AMT tax up-front on the exercise of your ISOs, it’s that you get to carry forward an AMT tax credit that can be used when you sell your shares. (You can even use a small portion of the credit in years when you don’t sell ISOs, as long as your AMT tax is less than your Regular tax for the year.)

Remember when we talked about cost basis above? And how it’s easy to report the incorrect amount of cost basis on stock options? Well…. ISOs don’t make things any easier, I’m afraid.

ISOs have a Regular Cost Basis and an AMT Cost Basis.

Let that sink in a moment.

This means that you need to track both cost bases because your Regular tax gain is computed differently from your AMT tax gain. This also means that in the year of sale, your AMT cost basis on a qualified disposition (shares held more than one year past exercise) is generally less than your Regular cost basis.

When your AMT tax is less than your Regular tax, the difference frees up AMT tax credits that you generated in the year of exercise. Any AMT tax credit that isn’t able to be used gets reported on IRS Form 8801 in the year after your exercise.

When we see errors in this area, it is often the result of switching tax preparation software (or switching tax preparers) from year to year.

Without your prior year tax information, it can be very easy to miss AMT tax credits, especially if the amounts are not very large relative to your other income.

And, if you’ve made it this far into the weeds with stock options, Congratulations! Here is one of the most important mistakes of stock compensation…

Mistake #5: Large Balances Due (and Interest and Penalties) at Tax Filing Time

After speaking with hundreds of stock compensation clients over the years, the most common refrain we hear (and why they are seeking out help for the first time) is a surprise balance due at return time.

After all, it feels like a ton of taxes are taken out of your paycheck already. Why is there still such a large balance due on your tax return?

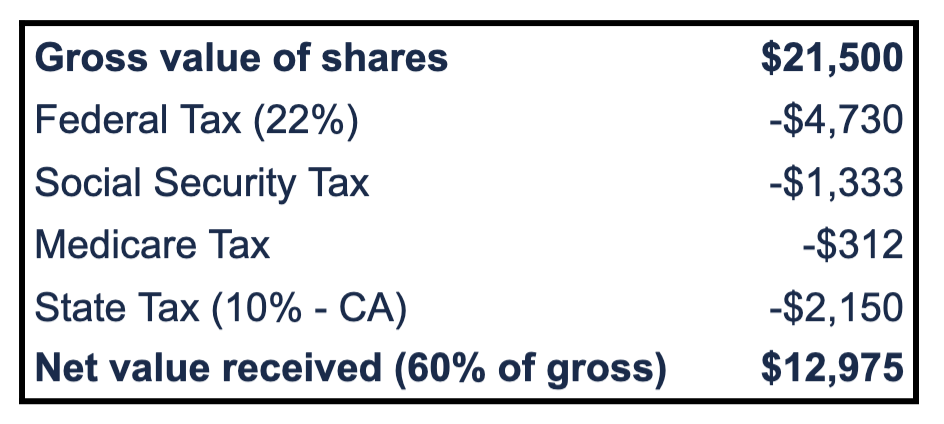

Let’s take a look at an example:

Alice has quarterly vesting of RSUs at Apple and receives 100 shares valued at $215/share in Feb 2023. Alice’s salary is $350,000/ year, filing as single.

Alice’s paystub shows the following:

Alice may be saying, “I already paid 40% tax on my shares, how is it possible that I owe more at tax time?!”

The key is that of the 40% withholding, only 22% is going towards Federal income tax.

And Alice is making $350,000 per year so she is in the 35% effective tax bracket. Alice is underwithheld on these RSUs by about 13%, which means a tax bill of another $2,795 come return time.

If you don’t budget for this, it can be a big blow at return time.

To make matters worse, if you receive other types of compensation—like bonuses, commissions, etc. (anything other than salary)—the IRS also requires employers to withhold federal income taxes at 22%.

The IRS considers all those types of compensation “Supplemental Compensation” and requires employers to withhold at a flat 22% regardless of the tax withholding elections you have in place with your payroll department for your salary. (Note: this withholding rate jumps to the top rate of 37% once your compensation is over $1MM for the year.)

Some tech companies are allowing their employees to elect a higher tax withholding rate on supplemental compensation.

Electing a higher tax withholding rate on RSUs, bonuses, etc., can help you avoid both a large tax bill at return time and the need to make quarterly estimated tax payments (which are a hassle, hard to compute, and easy to forget).

You may only have one shot to pick this rate at the beginning of the tax year, so watch carefully for any communication from your payroll department and work with your tax professional to determine the right level of withholding.

And a final note about interest and penalties…

It is important to understand your full year tax liability because the IRS will expect you to pay the correct amount of tax throughout the year

To avoid interest and penalties, you need to meet the lower of the following “safe harbors”:

- Pay 110% of prior year tax liability, or

- Pay 90% of current year tax liability

Most states have similar rules, but check your state to be sure.

If you haven’t paid enough throughout the year, the IRS can assess underpayment penalties and interest. You can easily avoid this with the right tax planning.

Tax reporting for stock compensation is not for the faint of heart, but with the right planning you can avoid the most common mistakes mentioned above.

If you’re new to stock compensation, please be sure to do your research or reach out to a qualified tax professional who regularly works with stock-compensation clients for help.

If you want to work with a financial planner who can help you make tax-aware decisions, and who can help connect you with other expert professionals (like CPAs!), reach out and schedule a free consultation or send us an email.

Sign up for Flow’s twice-monthly blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.