And in this corner, striking terror, hope, and confusion in parents’ hearts for years: College financial aid!

Have you been diligent in saving for your child’s college education? Does it matter? I’m guessing that very few of us will have saved up 100% of our child’s college’s sticker price. Enter financial aid. Part 1 teaches you how financial aid works enough so you can understand the whys of the strategies and tactics I’ll explain in Part 2.

How Financial Aid Is Calculated

To apply for financial aid of pretty much any sort (but certainly federal financial aid), you need to fill out the Free Application for Federal Student Aid (FAFSA). The information on that form is used to calculate your “Expected Family Contribution” (EFC), which is the amount of money the federal government thinks you should be able to put towards your child’s college expenses for that year. The less that the government or your kid’s school thinks you can afford to spend on college, the more money they might give you.

You re-apply for need-based aid every year, so you’ll have to pay attention to your income and assets for four years (or more! if you have more than one kid).

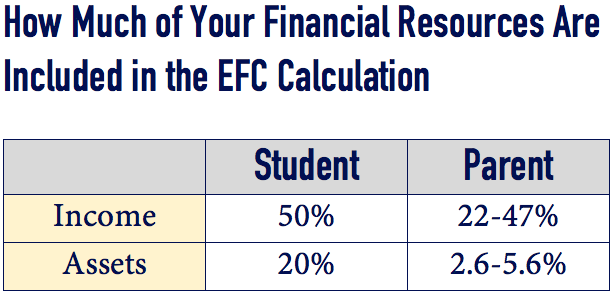

Expected Family Contribution

The EFC formula assumes that you and your child will be able to use the following resources to pay for college (source: savingforcollege.com):

Assets include 529s, investments, certain business interests, and real estate. Note that retirement accounts, cash-value life insurance policies, and tax-deferred annuities are not included. Also note that this is why I don’t generally recommend UGMA/UTMA accounts for college savings; the money is in the child’s name and therefore is counted more in the EFC calculation.

The primary strategy, then, is to reduce income, and then assets, especially your child’s.

FAFSA vs. CSS Profile

Many colleges use FAFSA in their financial aid calculations. Some also use the College Board’s CSS/Financial Aid Profile, which collects even more information than the FAFSA does. The CSS Profile is used by almost 300 colleges and scholarship programs to award financial aid from sources outside of the federal government. After you fill out the application, the College Board sends it to the colleges and scholarship programs you have chosen.

The big difference, especially for people in areas with expensive housing, is that the CSS Profile includes home equity. It also isn’t as helpful to divorced parents.

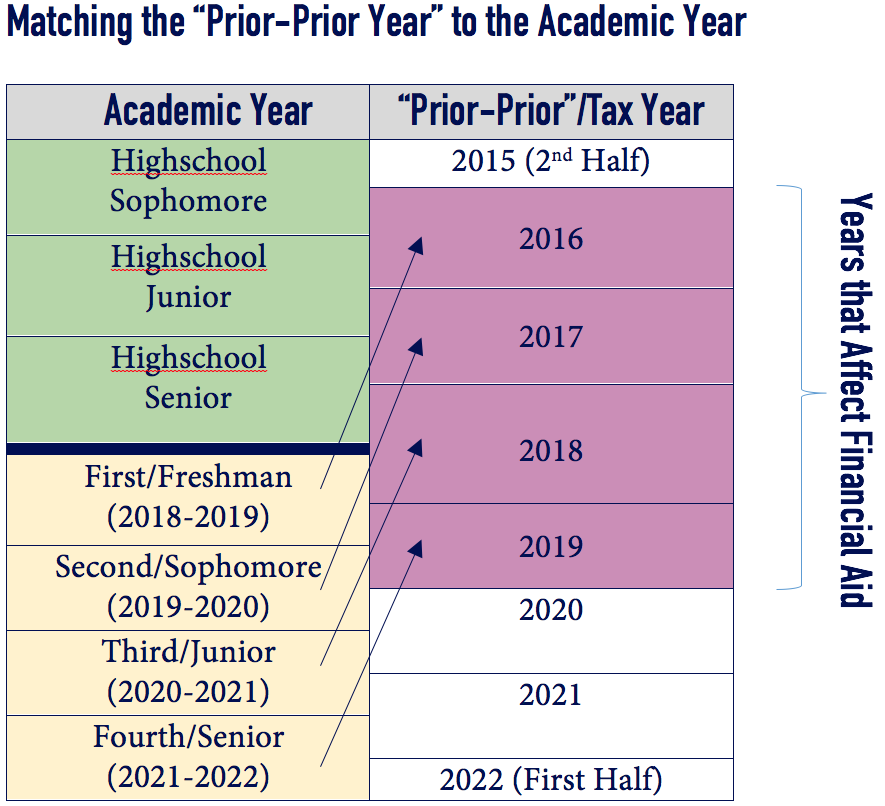

“Prior-Prior Year”

When you fill out FAFSA, you have to use data from a particular tax year. Starting this October, FAFSA is changing the rules about which year’s financial data you use. You will now use the “prior-prior” year’s tax-return data. For example, if your child plans to attend college in Fall 2018, you will use your 2016 tax return to fill out FAFSA.

Because the academic year the financial aid applies to and the tax year aren’t the same, coordinating the two can make your head hurt. Hopefully this graphic will be a useful reference for figuring out which tax year impacts your chances of financial aid for a particular college year.

5 Steps Towards Maximizing Your Financial Aid

- Before the middle of your child’s sophomore year in highschool (the first “prior-prior” year), start evaluating strategies for reducing your income and assets. Use this tool for an estimate of your Expected Family Contribution. You can tweak certain variables to test strategies available to you, and see what the effect is on the EFC.

- In your child’s senior year of highschool, apply for FAFSA, and apply early. Apply even if you don’t think you’re eligible. The only cost is a few hours of your time. You can fill out the form online and even import data directly from the IRS website.

It’s best to fill it out as soon as possible after January 1, since much financial aid is awarded on a first-come, first-served basis. To find out your exact deadlines, call the schools you’re applying to, and check resources like the general state FAFSA deadline list maintained by the U.S. Department of Education. - Determine if the school requires the CSS Profile and fill that out, too.

- Update your child’s college if your financial situation changes (you’re laid off; you have unexpected large bills) after submitting FAFSA and the CSS Profile. If your income or assets were anomalously high during a prior-prior year, explain that, too.

- Work with a financial aid consultant. Just like your financial “team” might include specialists such as an accountant, an estate planning lawyer, and an insurance agent, you can employ a financial aid consultant to drill deep into this aspect of your financial life. Then either you or your financial planner needs to coordinate the proposed actions with the rest of your financial life.

Involve Your Child

I am a fan of involving children in age-appropriate ways in all your major financial decisions. Teachable moments and all that rot. This is a perfect opportunity to involve your child: it’s a significant financial decision that directly involves them. Involving them might even save you some work. Your children can:

- Find out if the schools they’re interested in require the CSS Profile.

- Help fill out the FAFSA form and the CSS Profile.

- Use the “Net Price Calculator” for the colleges they’re interested in. This is a non-binding estimate of how much you’ll pay for the school (not the sticker price). You can find this calculator on every college’s website. For example, here’s the calculator for my alma mater. Net price allows you to compare apples to apples among schools.

And, of course, encourage your child to perform well academically throughout her entire highschool career to maximize chances of merit aid. Many elite private schools don’t award any merit aid, but state universities and not-quite-as-swish private schools might.

Resources

I saw a presentation by Paula Bishop, a Financial Aid for College Advisor, at a conference in February. She was entertaining and knowledgeable. At that time, she was charging $500 for help with financial aid applications. Imagine the possible return on THAT investment! (I have no financial affiliation with her and have not used her services.)

I’ve also used this website a lot as a resource. I am not familiar with it as a client, but it’d be worth checking out

Online Educational Resources

http://www.efcplus.com/financial-aid-award-letter-analysis/

https://bigfuture.collegeboard.org/?affiliateId=cbhomeexp&bannerId=bf

Read the next post in this series.

Do you want someone to guide you through the financial implications of your child’s college choice? Let’s figure it out. Reach out to me at or schedule a free 30-minute consultation.

Sign up for Flow’s Monthly Newsletter to effortlessly stay on top of my weekly blog posts and occasional extra goodies, and also receive my Guide to Optimizing Your Stock Compensation for free!

This article is provided for general information only, and nothing contained in the material constitutes a recommendation for purchase or sale of any security, or investment advisory services. Reproduction of this material is prohibited without written permission from Meg Bartelt, and all rights are reserved. Read the full Disclaimer.