In his column, “Everything You Know About the Crash is Wrong,” Zweig writes about the 90th anniversary of the stock market crash of 1929. More specifically:

- How we still don’t know what caused it. Even with 90 years of perfect hindsight to figure it out.

- How loooooong it took for the market to recover. It didn’t return to its 1929 level until…195-freakin’-4. Twenty-five years.

The column resonated even more than usual (he really is a good writer, so I consistently enjoy his pieces) for a couple reasons:

- A lot of my clients and other folks I run into are starting to ask about how to prepare for a recession. How to “recession-proof” their investments specifically and their finances more generally. When I started getting these questions a few months ago, I went ahead and wrote up my thoughts on how best to prepare for a recession.

- I had just recorded a video for my blog about using a “bucket” approach to investing, which could be appropriately used in preparing for a stock market crash.

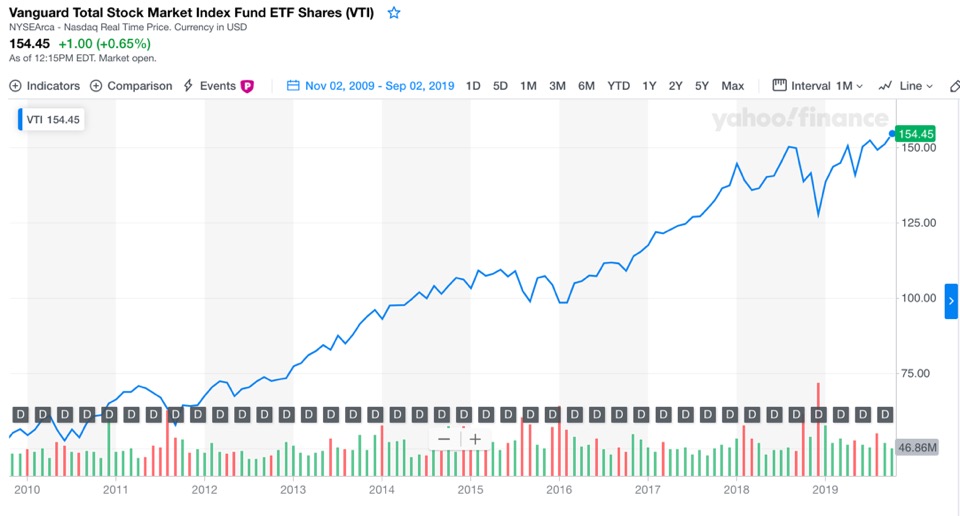

It’s been pretty darn easy to forget how painful stock market crashes can be over the last ten years. Because the market has gone up more or less continuously for that decade. To wit:

Chart generated October 28, 2019 at Yahoo Finance (Verizon Media)

What Should We Do, Then, If We Know a Crash Is Coming (Eventually)?

But a crash is a-comin’. When? Dunno. But it’s a-comin’. And I worry that we are collectively going to freak out and do exactly the wrong thing with our money when it happens.

But wait! This doesn’t mean you should just stockpile cash for the next 20 years of your life. It doesn’t even mean you should invest conservatively instead of aggressively. The stock market, on average, over time, goes up. And I want your money to go up along with it. Which means you have to have your money invested in the stock market.

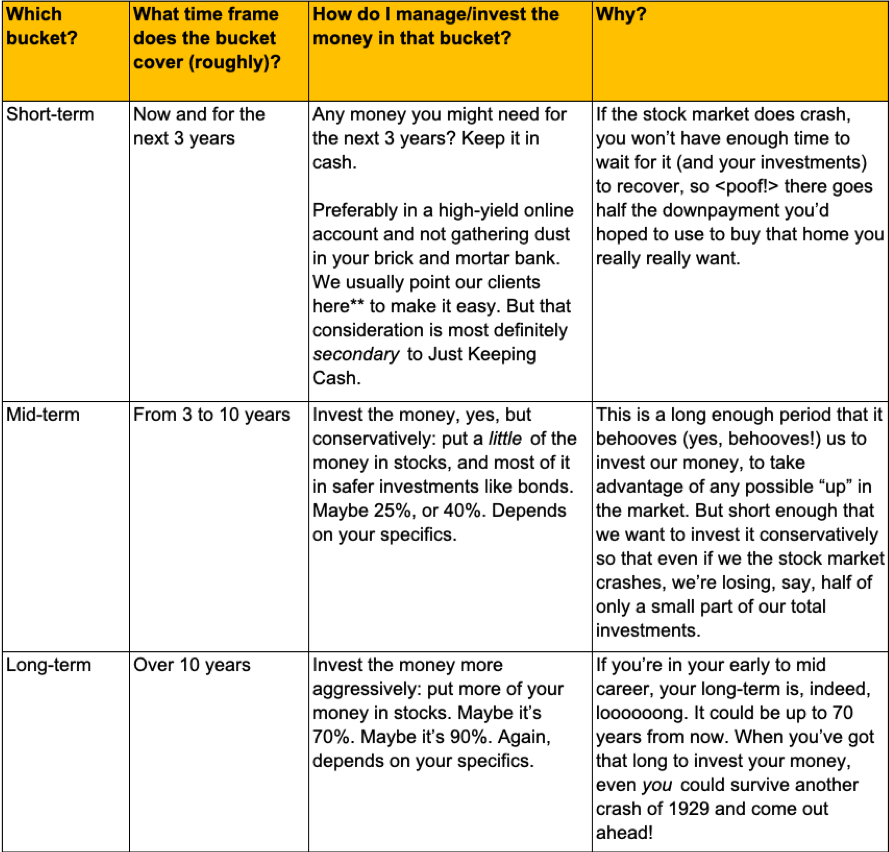

What it does mean is that you should be managing and investing your money in a way that’s tailored to:

- your time frame (do you need the money in 2 or 20 years?), and

- your ability to endure risk (are you going to look at your investment balance every day on Fidelity’s website? Or are you going to steadfastly ignore it until it’s gone?)

In theory, it’s all very simple: If your time frame is longer, invest the money, and invest it more aggressively. Shorter time frame? Keep cash or invest it conservatively.

So here’s where my recent video is particularly relevant, as it talks about a very specific method of doing just this. In it, I talk about using “buckets” to manage your money. I outright say that there’s no direct financial benefit to using buckets. But there is a potentially huge psychological and behavioral benefit. And when the market is crashing, it’s your behavior that will dictate how well you survive it.

The bucket approach to managing your money means to consider your money in several buckets, and manage those buckets separately. I usually talk about 3 buckets, but heck, I suppose you can really have as many buckets as you want. Just recognize that each bucket adds a bit more complexity and probably a bit of cost to the arrangement.

** https://www.bankrate.com/banking/

For those of you paying attention, I started by recounting that the stock market didn’t recover from the crash of 1929 for 25 years. And then I suggested that you can invest aggressively in the stock market for any time frame over 10 years. Ya got me.