As you might know, there’s a huge, all-encompassing change to tax law potentially coming up at the end of 2025. If it happens, you will almost certainly be big-time impacted.

What is that all-encompassing change to tax law? It’s the expiration of the Tax Cut and Jobs Act, which went into effect on January 1, 2018. All of the changes the TCJA ushered in will expire at the end of 2025—and tax rates and other rules therefore go back to the pre-2018 levels—unless Congress renews it.

It’s anybody’s guess whether Congress will renew it.

There are many provisions in the TCJA that really benefit our clients. If you, like our clients, are in tech, make good money and/or have good wealth, and have various forms of equity compensation, you probably benefit, too.

So, it behooves us to look at what tax rules are in effect now that potentially will disappear come 2026, and ask ourselves:

Should we take advantage of TCJA tax rules while they still definitely exist (because they might not exist come 2026)?

Consider these strategies this year and next.

Given the “maybe?” nature of all of this, you don’t want to do anything that you’ll regret if the tax laws stay the same. So, you’re looking for strategies that will serve you well—or at least not hurt you—regardless of what happens tax-wise.

This is, may I remind you, the nature of almost all of personal financial planning: You’re making decisions based on what you think or hope will happen in the future, not on what you know will happen in the future.

How do you still make good decisions in an environment of such irreducible uncertainty? For each choice available to you, you need to think about all the possible outcomes of making that choice. If any of those outcomes is simply unacceptable, then that choice isn’t right for you.

If some outcomes are better or worse than others, but none of them would be catastrophically bad for you (financially or emotionally), then it could be a reasonable choice to make.

For example, let’s say you work at a pre-IPO company. You have stock options. You could exercise them now, paying not only the exercise cost but also the associated tax bill. You can’t know what will happen to the company, and more specifically, the stock, in the future. Let’s say the stock does poorly and you lose all that money.

- If that means you’d lose your emergency fund and throw your retirement plans off track, then that’s not a reasonable choice.

- If that instead means you can’t take that One Vacation, but you’re more or less okay with missing it, then okay! Go forth and take that risk.

Below I discuss one strategy to consider before the TCJA expires (maybe): Roth conversions (and the corollary: contributing Roth instead of pre-tax). Later this month, I’ll publish another blog with the other strategies I think are worth considering:

- Exercising ISOs

- Delaying charitable contributions

- All sorts of potentially very complicated stuff to reduce the size of your estate (for those of you who already have millions of dollars)

I’m covering only those strategies that I think are most likely to affect our clients (and therefore you, if you’re like our clients). The changes made by the TCJA are vast and beyond the scope of this blog post.

If you want to know more about the whole TCJA “thing,” you can find articles that are broader in scope from the likes of Schwab or Forbes or any number of financial advisory firms focused on other clientele.

Why talk about this now?

The changes may or may not happen, and making giant decisions based on a possibility is often a bad idea.

But we’re talking about it now for a few reasons:

- There are some potentially powerful strategies you can use for 2024 and 2025 that will lose their power come 2026, if TCJA expires.

- If you need to involve an estate planning attorney in any work, they’re gonna be slammed come the latter half of 2025. Best to reach out to them ASAP.

- Even if it were entirely rational to wait for a while to discuss any of this stuff, you’re going to start seeing some “sky is falling” headlines, if you haven’t already. So, let’s discuss this in a useful manner before the headlines hijack your brain.

Roth conversions: Convert pre-tax IRA or 401(k) dollars to Roth

Why do we care about pre-tax and Roth?

Some background and edumuhcation about Pre-tax vs. Roth

Let me ask you a question: Would you rather save pre-tax when your tax rates are high or low?

The answer is High. If your tax rate is 39%, every dollar saved pre-tax saves you 39¢ in taxes. If your tax rate is 25%, every dollar saved pretax saves you 25¢. Saving 39¢ is better.

Now, would you rather save after-tax (i.e., to a Roth account) when tax rates are high or low?

The answer is Low. At a 39% tax rate, you pay 39¢ in taxes for every dollar you save to a Roth account. At a 25% tax rate, you pay 25¢ for every dollar you save to a Roth account. Paying 25¢ is better.

That’s a useful, but simplistic, way of thinking about the pre-tax vs. Roth/after-tax question. For a bit more nuance:

When you take money out of pre-tax accounts (typically IRAs or 401(k)s) in retirement:

- You will need to pay income tax on all of that money.

- That income can also increase other costs, like Medicare Parts B and D premium and the taxability of your Social Security retirement income.

- All money in a pre-tax IRA or 401(k) is subject to Required Minimum Distributions, meaning that you must take money out of those accounts starting at what is now age 73.

Sounds kinda crappy. Why would we put money into a pre-tax account? Why, to save money on taxes now, of course.

By contrast, Roth accounts are tax-free, and any money in those accounts can stay in there for your whole life, you never have to take the money out, and if you do, it’s not subject to taxes and won’t raise your taxable income in a way that will impact Medicare premiums, etc. But you don’t get any tax breaks now for any contributions or conversions into Roth accounts.

[Note: The “Roth vs Pre-tax” discussion is a multi-layered one. Some considerations are technical (comparing current tax rates with expected future tax rates). Some are emotional (I, for example, would rather just bulk up tax-free assets while I’m young and have strong earning power). This TCJA-inspired consideration has to fit into the larger Roth vs. Pre-Tax discussion, which is, alas! outside the scope of this blog post.]

Why now is such a good time to consider Roth conversions

I wrote a whole blog post about Roth conversions a little while ago. (If you think you want to do a Roth conversion, I highly recommend you read the whole thing. Oh, and work with a CPA to model the tax impact.)

In that post, I pronounced that one good opportunity for doing Roth conversions is when “You bet the federal government will raise tax rates.” Well….?! That’s precisely what we’re talking about here!

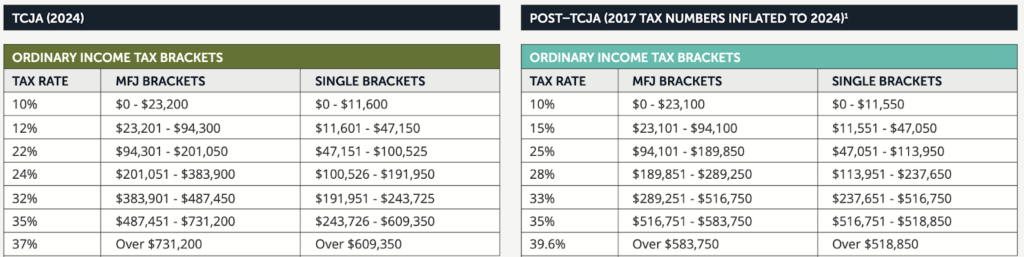

If TCJA expires, here’s how tax rates and tax brackets would change. Observe that not only do tax rates go up, but higher tax rates apply to lower bands of income, meaning that your tax bill could go up double-whammy style.

We already consider Roth conversions for clients who are having an unusually low-income year, clients who are taking a sabbatical, going back to school, got laid off and can’t find a job, etc.

Because of this TCJA thing, even if this is a totally “normal” income year, you should still look at doing Roth conversions. These might end up being anomalously low tax rates anyways, simply because of federal tax policy.

Keep in mind that doing a Roth conversion means you are volunteering to pay taxes before you have to. You could just wait for another several decades to pay taxes on this money. But you’re making a bet that by paying taxes now, you’ll pay less (over your lifetime) than if you pay taxes later. (So much delayed gratification energy going on here, it hurts.)

It’s always possible you could convert the pre-tax money, and the tax rates don’t go up. Lord knows there have been bountiful predictions for decades now that tax rates will (“have to!”) go up…predictions that have yet to come true.

Consider doing this: Ask your CPA to model for you how much you can convert from pre-tax to Roth (in your IRA or 401(k)) and still stay within the same tax bracket, or even one tax bracket up, along with the tax bill you’d incur in both cases. If you want to convert, remember you have to do so by year’s end. You can even convert some this year and some again next year.

Remember, you want to have cash or taxable investments to pay the extra taxes. You do not want to withhold any money from the IRA in order to pay the taxes.

Contribute Roth instead of pre-tax

Many of our clients have $100ks or over $1M in pre-tax accounts (IRAs or 401(k)s). That is a lot of money to consider converting. (In reality, it probably makes sense to convert only some of it.)

By contrast, annual contribution limits to all these retirement accounts are way way lower: $23,000 for 401(k)s and $7k for IRAs (plus some catchup for people 50 years old and up). So, “pre-tax vs. Roth contribution” can be a much smaller-scale decision.

It’s still worthwhile considering, however! And maybe, behaviorally speaking, it’s a lot easier to contribute Roth (and not reduce your tax bill) than it is to convert to Roth (and intentionally increase your tax bill, possibly by a lot). Progress, not perfection, people!

Many of you likely have access to, and perhaps are even saving to, after-tax contributions to your 401(k) (aka, mega backdoor Roth). In that case, you’re already getting lots of after-tax/tax-free money into your retirement portfolio. Maybe that takes the pressure off shifting even more money into that tax-free status.

Consider doing this: Saving to your 401(k) Roth instead of pre-tax, for the rest of this year and in 2025. You could switch back to saving pre-tax if TCJA expires and tax rates jump up.

It’s hard to figure out how all this affects you!

I don’t know if you’ve noticed this, but our federal tax code is complicated. Like, really, really complicated. And getting more so every year. (Be sure to give your friendly local CPA a sympathetic glance, and maybe a cookie, next time you see them.)

The tax code is so intricate and interrelated that you can’t ever glibly proclaim that the change of <this one thing> will affect your taxes <in this specific way>. You need tax software because you need to effectively process your entire tax return in order to get a reliable answer about any single thing. It’s an unfortunate reality.

For example, if you live in California and have a mortgage and earn a lot of money, the higher tax rates will hurt you, but your ability to deduct more of your mortgage and more of your state income taxes (as illustrated below) will help you.

Source: fpPathfinder®

To make good decisions confidently, you need to work with a tax professional who has software that can model your entire tax situation under TCJA tax rules vs. your tax situation if TCJA expires.

Alright, friends and strangers. See you in the next blog, for more discussions of strategies you should start considering before the end of this tax year. Tootles.

Would you like to work with a thinking partner who can help you to discover and define your goals, and use that to help make your best financial decisions? Reach out and schedule a free consultation or send us an email.

Sign up for Flow’s twice-monthly blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.