Do you ever feel that your cash flow should be easier to get a hold of? You should be able to automate it? Not have to think about it so much? Not have to move money around with your delicate hands so often?

But, as it turns out, you just don’t find it simple. So you don’t get a handle on it. And you’re left letting your cash flow sort of happen to you instead of you managing it intentionally. And then you slosh money from account to account with the discomfiting notion that “This is stupid. I know I’m not doing this right.”

Many of my clients have just that challenge with their cash flow. And it is indeed possible to add structure, automation, and comfort to it!

In this blog post I’m going to focus on the income and savings part of your cash flow, not the spending side (which, in practice, is way way harder because it’s so tied up with our emotions and habits).

And furthermore, this is a tactical discussion, not philosophical. I’m not going to talk about the “Why” of saving and spending. As with all important decisions in life, tactics should follow your “Why.” You can optimize the tactics all you want, but without an overarching “Why,” you’ll only achieve your bliss by accident.

But because the actual implementation is what hangs people up so often, let us forge ahead!

Why Is It So Hard?

I suspect that most of us probably imprinted on our parents’ experience, which seemed simple and straightforward. And it probably was! Your parents probably had a salary…and that’s it. If you have a salary, you receive the same income in every paycheck, month after month. That makes planning pretty easy.

Your Income Streams are Multiple and Variable

So, let’s see what your income looks like. If you’re an employee in a tech company, you’ve got

- A salary.

- Maybe a bonus, once a year, maybe twice a year

- If you’re lucky, you get Restricted Stock Units that vest every month, quarter or year.

- And maybe you participate in your company’s Employee Stock Purchase Plan that gives you company stock (which, of course, you turn into cash ASAP. Riiiiight?) every 6 months.

If you have anything beyond a salary, or maaaaybe a salary + bonus, it gets a lot harder to stay on top of your cash flow. Try being a couple, where there are two sets of convoluted income streams, and at the end, 2 sets of individual spending and saving goals and one set of joint spending and saving goals.

You Can’t Automate A Lot of It

One of the biggest reasons it’s hard to get on top of your cash flow, and especially your savings, is that you simply can’t automate a lot of this.

Let’s say you want to save some money. You can easily set your paycheck to automatically contribute:

- to your 401(k). In fact, “from your paycheck” is the only way to save to your 401(k). And

- say, $200 to an investment account (which you should be doing…at some dollar level)

Set it and forget it. The eternal way.

But that works well only if your income is the same amount every time.

- What happens when those RSUs vest, and you sell them for cash (or rarely, they’re “settled” in cash initially, not in stock)?

- What happens when the ESPP purchase period is over, and you sell all the company stock for cash?

Now maybe you’ve got an extra $5k, $10k, $50k of cash sitting in your brokerage account (the account where your company’s stock plan is administered…a Fidelity account or E*Trade account or or or). You’ve got lots of cash above and beyond your 401(k) contribution and $200 contribution to an investment account.

You can’t automate that primarily because the value of the company stock (and therefore of your vested RSUs and ESPP shares) will continually change based on the price of the stock. So we can’t know until day-of how much cash your RSUs or ESPP shares are worth and therefore how much we can transfer to another account.

Is It Really So Bad to Not Have a Handle on My Cash Flow?

Well, as you likely already realize, it feels bad to not be in control of your money as it flows through your life.

On top of that (which is enough in itself!), I can think of two other reasons why this is, uh, less than ideal:

- if you can’t stay on top of it, chances are you’re spending more than you should…and more than you realize…and on things you’re not really even that aware of or that you don’t value that much. Which in turn means you’re likely not saving as much as you could (pretty effortlessly) be saving.

- Very likely that cash is just gonna sit around in your brokerage account, being all chill and “hey, man, I’m cash…not earning a damn thing.” instead of you investing the cash or using it in a more intentional way. Inertia is strong, my friend.

How to Get A Handle on Your Complicated Cash Flow

It’s NOT simple. It IS complicated. It IS hard.

And also, if you spend some time thinking (yes, kinda hard…but just one time) about your financial situation, you CAN set up a plan that:

- is (largely) automated

- gives you much easier understanding into how money is moving through your life, and

- gives you confidence that you’re saving and spending appropriately.

Here are a couple of examples from my clients (anonymized, obvs) that demonstrate how you might analyze your cash flow situation and come up with specific tactics for yourself.

Example 1.

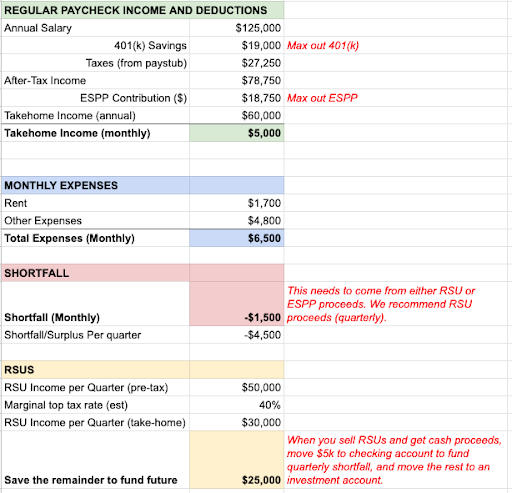

Client situation: Single, 20-something woman in tech. She has a salary, RSUs that vest every quarter, and an Employee Stock Purchase plan whose purchase period is 6 months long (i.e., it turns her cash contributions into company stock in her account every 6 months).

What’s the challenge? We want her to max out her 401(k) (for the tax savings and of course to get closer to financial independence) and to max out her ESPP participation (“free money”). Those have to come out of her paycheck. Take away taxes and she’s left with $5k every month take-home, in a regular month. Alas, she needs $6500 every month to cover expenses. She has a $1500 monthly shortfall.

Where will that money come from?

And what do we do with the ESPP shares (which she sells and turns into cash) she receives at the end of every 6 months?

The solution: We decided to use her quarterly RSU proceeds to subsidize her monthly spending. Every quarter, at the company stock’s current price, she should take home $30k after-tax. So, every quarter, she will move:

- $5k to her checking account (that she lives out of, to subsidize her monthly spending for 3 months) and

- $25k to an investment account.

This, alas, cannot be automated, for the reason stated above: We don’t know for sure what those vesting RSUs are going to be worth until they day they vest, because stock prices change moment to moment.

So, we put a reminder in our systems to reach out to her on the vesting day of each quarter and:

- Remind her to sell all the RSUs (and offer to hop on videoconference with her if she wants some company in navigating what are often stupidly confusing interfaces)

- Ask her how much money that is

- Remind her to move $5k to her bank account and the rest to her investment account

And remember she’s also got that ESPP that produces a whole bunch of company stock in her account every 6 months. This ESPP money is all “gravy” to her as we’re covering her expenses with other income. So, we want to save it all towards her glorious future (whatever it ends up being). So, every 6 months, we reach out to her and:

- Remind her to sell all the shares she received and pay taxes on it (are taxes auto-withheld or are estimated payments necessary?)

- Ask her how much money that is.

- Remind her to move all of it to her investment account.

You could do the same yourself, with some initial analysis, reasonable calendar rigor, and sufficient dedication to not letting this stuff slide. (And you know, a bit of rejiggering every time your income changes.)

Here’s what the initial analysis might look like:

Example 2.

Client situation: Married couple with a baby. Both working full time, with a salary, 401(k), Employee Stock Purchase Plan, and a Health Savings Account (HSA).

What’s the challenge? They can pay their “normal” monthly expenses out of their normal paycheck, even after maximizing all those paycheck contributions (401(k), HSA, ESPP).

However, they have several significant goals that they can’t save for from their regular paycheck, after all those deductions. How will they fund their kid’s college savings plan and a house upgrade, as well as the all-purpose “Opportunity Bucket.”

[Side bar: What is an “Opportunity Bucket”? It’s a concept I use with a lot of my clients to think about what life might be like in 5, 10 years. That’s certainly not “Retirement” for most of my clients, as they’re in their early to mid-careers. But most people think only about saving cash for “now” and investing for “retirement.” What happens to the 20, 30, 40 years in between? Or just the next 5 or 10 years? We want to save and invest towards that time in your life, even if you don’t know what’s going to happening then. Sure will be nice to have money sittin’ around when you do figure it out. And that bucket of money is your Opportunity Bucket.]

The solution: We set their paychecks to max out their 401(k)s, their HSAs, and their ESPP. Then we set a reminder every 6 months (when the ESPP’s purchase period ends) to sell all the company shares, pay taxes on the income, and then push a certain dollar amount into each of their goals:

-

- $x into their kid’s 529 plan

- $y into their house upgrade account (cash account)

- Whatever’s left into their Opportunity Bucket (investment account)

Again, dealing with the ESPP proceeds is not something they can automate. But having done the analysis ahead of time, it doesn’t take much time or thought process. So in a few minutes they can do the necessary (simple) arithmetic and then move the money from their brokerage account (where the ESPP proceeds are) into the various accounts listed above.

How to Apply This to Your Cash Flow

So, if we can generalize from these two examples, here’s a process you could use:

- Set your paycheck savings (ESPP, 401(k), HSA, etc.), which will happen automatically.

- Figure out how much money you need for regular, monthly living.

- Does your now-reduced take-home cover your regular, monthly living? If so, great!

- All the other forms of income (RSUs vesting, ESPPs, bonuses) can be divvied among your various goals and accounts, manually, when you actually get that income.

- Set a recurring calendar reminder for yourself for the days when your RSUs vest or your ESPP purchase period ends.

- If not, then figure out how much more income you need on top of your regular paycheck take home to cover your expenses. Let’s say your shortfall is $1k.

- When your get those other, irregular, unpredictable, or infrequent sources of income, put enough of it into your bank account to cover that shortfall.

- If your RSUs vest every 3 months, you’ll need to put $3k into your bank account every time RSUs vest. If you’re relying on your ESPP, and its Purchase Period is 6 months long, you’ll need to put $6k into your bank account every time you get your shares and sell them for cash. You get the picture.

If this seems like a lot to figure out and implement all at once, it probably is. So just try imparting a bit of structure into your cash flow at first. See how it feels. What works for you. What doesn’t. And just tweak every month for a while until it feels easy and you feel in control. At which point, VICTORY!

Do you want help figuring out how best to stay on top of your complicated cash flow? Reach out to me at or schedule a free consultation.

Sign up for Flow’s weekly-ish blog email to stay on top of my blog posts and videos, and also receive our guide How to Start a New Job (and Impress Yourself and Everyone Else) for free!

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Meg Bartelt, and all rights are reserved. Read the full Disclaimer.