How many of your RSUs should you sell when they vest?

I have long given the advice, “Just sell ‘em all, ASAP.” But I’ve grown a bit soft in my old age (hush your mouth).

I’ve worked with a lot of clients with RSUs, and I hear stories from other colleagues with their own similarly situated clients. We all know that “sell ‘em all, ASAP” sometimes isn’t good advice simply because our clients won’t follow it.

So, I am willing to entertain that you might hold some shares…and that’s not necessarily the end of the world.

Important Note! There is no tax reason to hold on to vested RSU shares. You incur the full tax liability the moment they vest. You can’t affect that tax bill with your “sell or hold?” decision. The only reason to hold on to the shares is an investment decision: You think this stock is going to outperform other stocks and the stock market in general.

If you do not want to or otherwise cannot bring yourself to sell all of them—or maybe you just want to think about other approaches—here’s how I talk about it with our clients.

(For simplicity’s sake, I’m talking about regular ol “been public for at least 6 months” company RSUs, not companies that just IPOed and are in some form of lockup.)

The Conservative and Best-on-Average Approach: Sell ‘Em All

On average, across all RSU recipients and all market conditions, aka, statistically, this is the best answer. The reasons are numerous. Here are the two best:

- Let’s say your RSUs are worth $100,000 when they vest. If I gave you $100,000 in cash income instead, would you go out and use that money to buy your company stock? If your answer is No, then that is literally the same, financially, as selling all your RSUs.

- Investments that are diversified—your money is invested a little bit in a lot of different stocks or bonds—perform better, on average, than investments that are “concentrated” in one stock. Diversification is said to be “the only free lunch” in investing. Keeping your company stock is anti-diversification.

You’re better off selling them all and:

- Using the money immediately for some current need (ex., downpayment) or other financial opportunity (ex., paying off debt), or

- Investing the money in a broadly diversified, low cost portfolio

The Riskiest Approach: Sell Nothing Beyond the 22% Withholding

Now look, I acknowledge that in the last few years, especially with certain high-profile companies (I see you, Amazon and Netflix), holding on to as much company stock as you can has produced More Money for you. Because the stock price has only gone up.

Add on top of that, if you work for a company, you have some insight into what your company is doing and therefore believe you know better than all the other investors out there how your company’s stock will perform in the future.

That makes my fundamentally conservative argument a little hard to sell. I get that. But it’s also my job to think about “Just how could this—for any value of “this”—blow up in your face?”

If you are keeping a bunch of company stock, you are—consciously or not—relying on the truth of the old investing saw: Concentration Builds Wealth; Diversification Protects Wealth.

You think—again, consciously or not—that by holding on to your company stock (concentrating), it is going to grow enough more than the broader stock market to meaningfully change your life. There is literally no other reason to hold on.

And you know what? It might be acceptable to take this bet. If…IF:

- You have your financial cash cushion (your emergency fund), and

- You have identified and funded the essential parts of your life (ex. Your rate of saving to your 401(k) will still allow you to retire at a reasonable age, or you’re otherwise on track to save for for your kid’s college…whatever goals are Non Negotiable for you), and

- You’d still be okay if this company stock evaporated in the future

Statistically, it likely won’t work. But owning a single stock is one of the only ways you have a chance of getting life-changing returns in the shorter term. (In the long run, “simply” saving enough and investing reasonably will change your life.)

Note that it’s not owning your specific company stock that gives you this chance. It’s that it’s a single stock of any sort…you could sell all your RSUs and invest it all in Bitcoin! Or Coca Cola! Or Berkshire Hathaway! It’s the concentration that’s key, not the “your company-ness” of it.

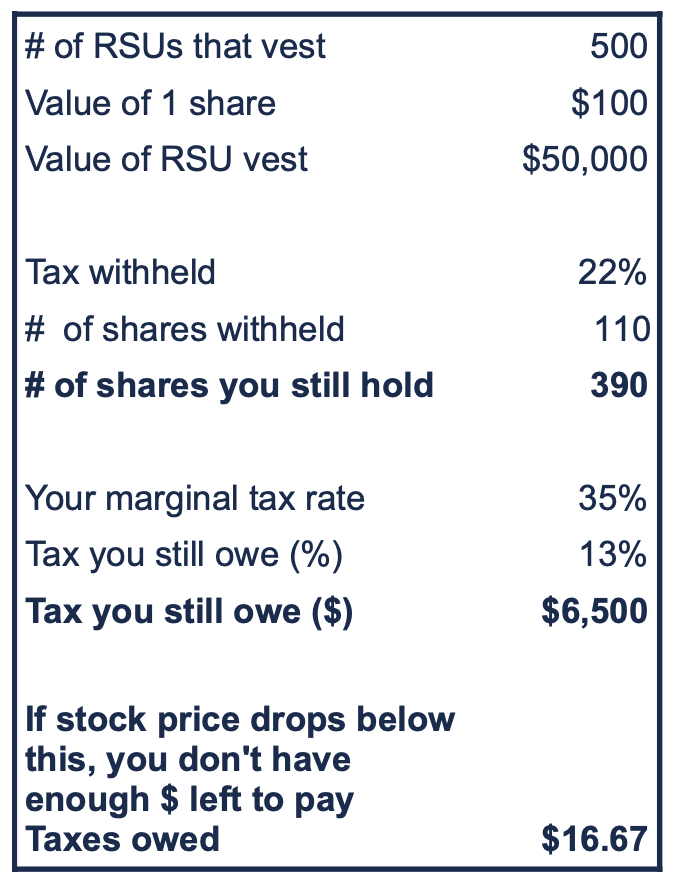

At Least You Can’t Lose Money: Sell Enough to Fully Cover Taxes

The worst case scenario with RSUs, in my opinion, is that you lose money on them. And that’s a possibility if you do not sell enough RSUs immediately to pay your full tax bill.

How could that happen? Hopefully you can follow these numbers. The bottom line is that, if the stock price drops enough after the initial 22% withhold, before you sell more to pay your taxes, then the shares you still have can be worth less than the taxes you still owe.

Back in the first Dot Com boom, or rather in the Dot Com Bust, this phenomenon bit people in the butt when it came to non-qualified stock options. (RSUs weren’t common back then.) They exercised NSOs when the stock price was soaring, incurred a hefty tax bill upon exercise, didn’t sell the resulting shares, and by the time tax time came around, the price had fallen a lot and they had a hard time paying their tax bill because their stock was no longer worth enough to cover it!

Except in rare circumstances, your company is going to withhold only 22% of the RSU income for federal taxes. Most likely, your tax rate is higher than that. (Check out tax rates here.)

If you’re working with a CPA or other tax professional (usually a good idea), you can ask them to calculate how much tax you owe. If you want to back-of-the-napkin it yourself, you can do the calculation in the table above (making your best guess as to what will be your marginal/top tax rate this year). In the example above, you’d sell another $6500 worth of RSUs and pay it to the IRS.

Somewhere in Between: Sell More Than Taxes Require but Hold Some

In the spirit of being complete, I’d just like to add that there’s an almost infinite spectrum of decisions you could make here. It’s not just the three options I describe above.

I find this cognitive flexibility comes in handy when I’m working with clients whose net worth is tied up heavily in their company stock. In my profession, there’s a rule of thumb that no more than 5% of your investment portfolio should be in a single stock. Often I work with clients who have 20%, 50%, 90% of their “liquid” net worth (i.e., cash and investment accounts) in their company stock.

I recognize the frequent uselessness of saying “Let’s sell it all the way down to 5%!” It’s just too big a shock to the system. But I find most people are fine going from 90% to 70%. Or 50% to 40%. And you know what, that’s progress towards a portfolio whose “risk-adjusted return” is optimized.

I hope this post helps “unstick” you a bit when it comes to making decisions about your RSUs. Remember, “sell ‘em all” is always a prudent choice (and that holds true even if the stock price ends up rising!).

Do you want to work with a financial planner who knows the rules, and who can also adapt to your specific personal, emotional, and financial circumstances? Schedule a free consultation.

Sign up for Flow’s weekly-ish blog email to stay on top of my blog posts and videos.

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Meg Bartelt, and all rights are reserved. Read the full Disclaimer.