I rarely talk about investing in this blog. It has been on purpose.

There are three reasons:

- Investing is boring.

At least, if it’s done right. If it’s exciting, it ain’t investing. It’s gambling. Also, the rest of your finances and your life are not boring. Let’s talk about those instead! - There is so. much. more. to your financial life than investing.

You often have many more things to think about and many more decisions to make for those things. - Everyone and Everything Else talks about investing and the infinite number of investment considerations you can think about (not necessarily that you should think about) when it comes to your investing, and it’s annoying.

Industry thought leader Carl Richards coined the phrase “the financial pornography network” to describe all the many voices and media channels and financial companies out there talking about investing minutiae non stop…because it’s to their benefit if you think about it nonstop.

That said, I have realized that I have gone a little too far in the other direction and talk about investing too little. Because as soon as you have a dollar invested, investing becomes important to you. And the more dollars you have invested, the more important—both numerically and psychologically—it becomes.

Mea culpa.

So, let me start to make up for that omission by discussing our investment beliefs here at Flow (which are also my own personal beliefs, which I use with my family’s investments).

I will intentionally stay at a fairly high level in this blog post. Why not go into implementation details?

- This is a blog post, not a college course.

- There are multiple ways to implement. As Mike Piper, a financial planner, financial writer, and CPA, says, “There is no perfect portfolio. There are plenty of perfectly-fine portfolios.”

- I firmly believe that once you understand your beliefs about investing, the actual doing of investing is more a matter of diligence and rote application than figuring out something complicated.

Not at all coincidentally, it is also the case that once your understand your personal values and aspirations, the easier the personal financial decisions are to make and implement.

Our Investment Beliefs

When I started writing this blog post, I wrote that “we abide by a few but strongly held beliefs when we invest our clients’ money.” As I started thinking about it, and writing down what those beliefs are, it turns out they’re not so “few.” Thankfully, I don’t think any of them should be surprising or complicated.

First, know what you’re investing for.

What are your goals? When do you want this goal to happen? How much money will this goal require (if you can estimate)?

Understanding (as best you can) what your goals/dreams/intentions are is perhaps the most important and helpful part of investing well.

The timeline, the amount, and the “need-to-have vs. want-to-have” nature of a goal will dictate how much of your money you stick in high-growth/high-volatility investments like stocks, and how much in low-growth/low-volatility investments like government bonds.

- Are you 35 and looking to retire eventually and then live off that money for the rest of your possibly-7-decades-more-of-life ? You should probably be invested mostly in stocks.

- Are you aiming to buy a home in 5-10 years? Well, you should probably invest that money more in lower-volatility investments like US government bonds with short durations.

- Are you hoping to buy a home in 1 year? You likely need to keep that money as cash or equivalent.

I will now proceed to list the remaining beliefs in no particular order. I tried to figure out an order, really, I did. But I kept on changing my mind about if this one were really less important than this other one and so, for the sake of my mental health, declared them all my favorite children. (Unlike with my actual children…)

Keep costs low.

You can find a million different articles, graphs, and charts about this on the internet. Here’s one from the SEC itself, illustrating the effect, over 20 years, of investment costs of various levels. The basic message is:

The higher the costs, the less money you have in the end, all else equal (a phrase which sometimes can do a lot of work).

You can keep costs low in several ways:

- the investment itself (all funds have “expense ratios,” for example)

- investment-management services

- transaction fees (ex., does it cost money to buy the stock or fund?)

- other “how capital markets operate” sausage-making costs that are too convoluted for here (ex., bid-ask spreads in ETFs)

Own the market. Don’t try to beat the market.

Basically, no one can beat the market (and here’s the important part) consistently and over years.

This means owning stocks. US and international. And bonds. US and…international is always up for debate. And real estate.

Own eeeeeverything [please note: hyperbole at play; boring, non-hyperbolic version = “own a wide variety of investments”] and don’t try to figure out when you should or shouldn’t hold this bit or that bit. #YoureJustNotThatSmart #ButDontWorryNoOneElseIsEither

What I’m describing is “diversification.” Own some of everything.

One of my favorite sayings about investing is “Diversification means always having to say you’re sorry.” Why? Because if you own some of everything, something you own is always going to be performing worse than everything else. It’s gallows humor for investment nerds.

At the same time, diversification also means always being able to declare yourself an investing genius because you always own the investment that did the best, too. But no one consistently knows what the best or worst will be ahead of time.

I have an undergraduate degree in Economics. I knew enough about academic economics by graduation to know that I didn’t want to pursue it at the graduate level. Fast forward 10 years, and I’m sitting in a chapter meeting of the San Francisco Financial Planning Association, on the 50th (51st?) floor of the Bank of America building, listening to a BofA economist address the group.

I remember only one thing he said (and I paraphrase): “I love being an economist. When I make a projection that turns out right, everyone thinks I’m a genius. When my projection turns out wrong, everyone forgets about it.” Truer words…

Watch your behavior.

You can be super smart and think intelligent things…but if you don’t have discipline and you do bone-headed things, your investments will suffer.

Did you pick out a balance of stocks and bonds that is appropriate for you? And you picked out some reasonable funds to help implement that strategy? Great!

You can sink it all if you then let fear and FOMO drive you to sell after the stock market has fallen 30% and buy after it has recovered and reached its peak again. Which is really tempting at times, let me tell you.

Here’s a slightly outdated article (from 2018, but the point remains) that shows you the impact of missing the 10 best, up to 60 best, days in the stock market between 1999 and 2018.

Your average annual return would have gone from 5.62% to 2.01% if you’d missed the 10 best days because you were trying to figure out the best time to put your cash into (or back into) the stock market.

Minimize taxes.

On the one hand, duh.

On the other, there’s nuance to it.

We want to minimize taxes over time, not necessarily within any single tax year. Sometimes we intentionally incur taxes now to save even more taxes later.

Also, we don’t want to minimize taxes to the detriment of the investment portfolio. We make good investment decisions first, and optimize for taxes second. (Ye olde adage of “Don’t let the tax tail wag the investment dog.”) A great example of doing it the wrong way is to not sell company stock (which makes up 75% of your total investment portfolio, a very risky position to be in) solely because you’d have to pay a lot of taxes on the sale.

We look at what the ideal investment moves would be, then we look at those moves through a tax-minimization lens to see if there are reasonable tweaks we can make in order to reduce taxes.

For example:

- Can we sell different shares of the company stock, because those shares have a higher cost basis and will therefore have a smaller, taxable gain?

- Can we sell some of the shares this year and push some into next year so that some of the gains are at a lower tax rate?

- Can we sell some investments at a gain this year and intentionally incur taxes, because you’re on sabbatical and your income is low, which means the tax rate on your investment gains will be lower?

Use “Asset Location”

Another way to minimize taxes is to employ a bit of “asset location,” meaning, at its simplest, that you put:

- investments that generate taxable income each year (ex., bonds) into an IRA, because that IRA “wrapper” means you don’t have to pay any taxes on any money while it’s still in the IRA

- tax-efficient investments (like a total US stock market fund) in a taxable account, because although you’ll owe taxes on investment income, there won’t be much of it

- high-growth investments (like stock) in a Roth IRA, because that has the best chance of growing into a lot of money, and you don’t owe taxes as it grows or when you take the money out

You can get really deep in asset location, but if we’re balancing “simplicity” with “tax minimization,” I believe these are the three most important rules to keep in mind.

Don’t obsess about specific investment choices.

Sure, we (necessarily) use specific funds in our clients’ portfolios. But there are lots of good funds out there: broadly diversified (“own the market”) and low cost.

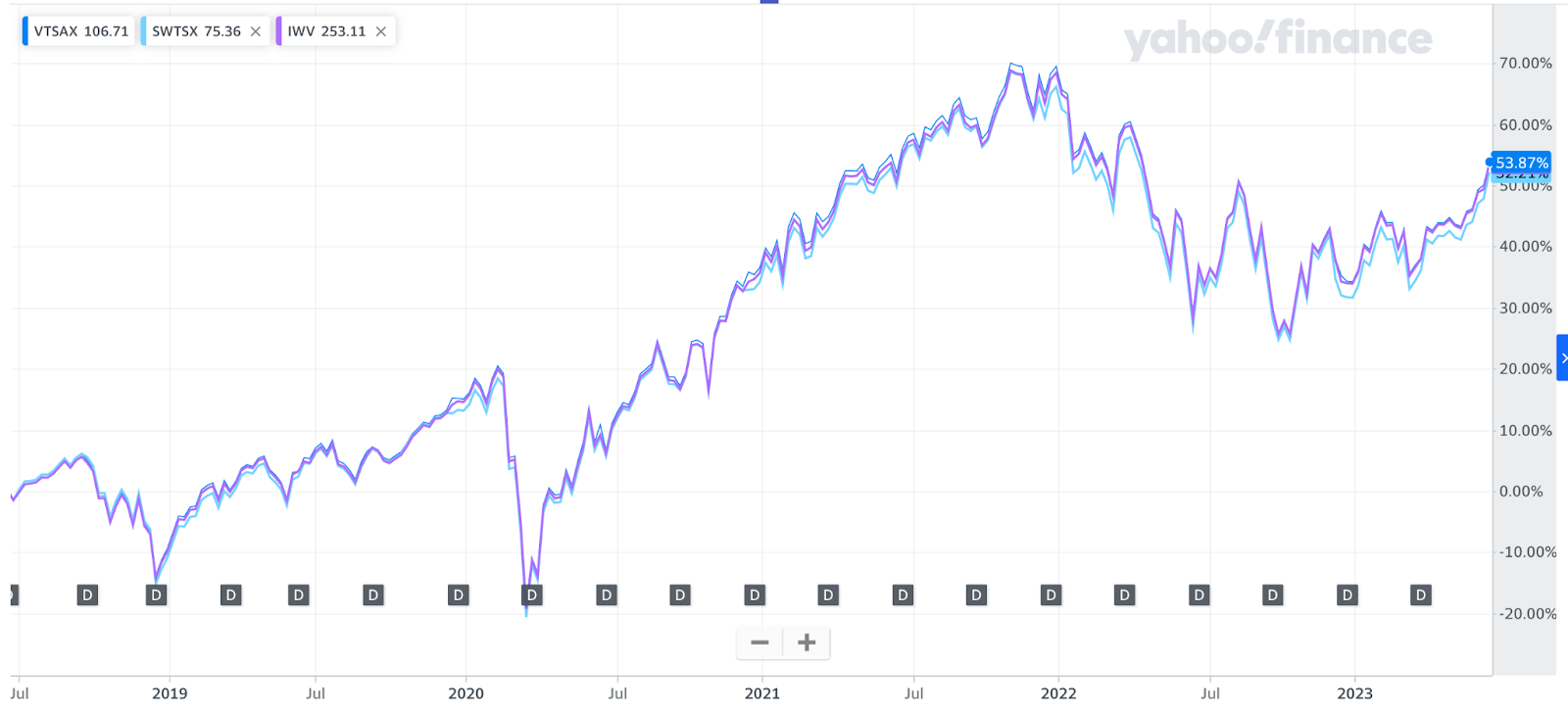

For example, if you wanted to own the US stock market in one fund, you could consider any of these total-US-stock-market funds: VTSAX, SWTSX, and IWV. (This isn’t an endorsement of any of these funds. I’m using them to illustrate how similar different funds can be.)

While they aren’t identical (they have slightly different costs, they track different indexes), look how similarly they performed over the last five years:

Source: Yahoo! Finance, 6/20/2023

Control What You Can. Ignore the Rest.

You simply cannot control what the various markets (stocks, bonds, crypto, real estate, commodities) are going to do.

Nor can you control what the Fed is going to do with interest rates, how the economy is going to perform, whether the tech market is going to explode or implode, how your company stock is going to perform, etc.

So, there is no benefit—and plenty of detriment—to managing your investments with the idea that you can control (or predict!) those things.

What can you control? What is worth your time, effort, and focus?

The things I discuss elsewhere in this blog post:

- Costs

- Your balance of stocks and bonds (aka, your “asset allocation”)

- How much you save towards your goals

- What you buy and sell

- When you buy and sell it

Fight for simplicity.

Fight for simplicity. In the investments you select. In the number of accounts you own. In the number of companies (Robinhood, Schwab, etc.) you hold your accounts at.

Every choice you make, consider it through a lens of “could this reasonably be made simpler?”

Why is simplicity so important?

- You can actually understand how you’re invested.

- You can figure out how your investments are performing more easily.

- You’re less likely to get snookered into investing in something that’s “hot” at the moment.

- You’ll spend less time and stress on your investment portfolio. At this stage in my life, I think this might be the most important thing.

- Gathering all your documents for your tax return will be, if not easy, then less onerous.

Despite the fact that we haven’t historically talked a lot about investments in this blog, it’s so very important that you should understand how your money is invested and why.

You should ideally get clear on what your investment beliefs are, so that you can ask yourself “Is this money being invested according to my beliefs?”

Whether you’re investing your money on your own, using a robo-investor (ex., Betterment) to do it, or working with a financial professional to do it, the answer should be “Yes.”

Do you want to work with a financial planner who can help you manage your investments according to these beliefs? Reach out and schedule a free consultation or send us an email.

Sign up for Flow’s twice-monthly blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.