A curious thing is happening when big tech companies, like Lyft and Uber, go IPO nowadays. I mean, aside from the fact that their stock immediately starts losing value…although that figures into my point, which is:

Your RSUs might be vesting on Day 1, not after lockup expiration. And that creates a tax hassle and possibly a big investment risk for you.

That’s my gentle description. To my colleagues, I’ve been describing these companies’ decisions around RSU taxation as “a real d*ck move.”

You can’t change how your RSUs work. But you can at least make sure you don’t get tripped up by your tax obligation.

How Private Company RSUs Should Work During an IPO (in my opinion)

In my previous blog post about RSUs in private companies, I talked about the idea of double-trigger vesting:

the shares aren’t really truly yours until[…]:

1. The vesting date arrives, and

2. The company goes public (or some other liquidity event that would enable you to turn these shares into money)

Why is double-trigger vesting important? Because “If your RSUs vest when your company is still private [aka, single-trigger vesting], you’ll owe taxes but not be able to sell the shares for the money you’ll need to pay the taxes.”

So, nicely enough, companies like Uber and Lyft included double-trigger vesting in their RSUs. According to those rules:

- When you passed the vesting date but the companies were still private, you pretty much “owned” the RSUs and could leave the company, but the shares weren’t yours yet for tax purposes.

- You waited until the company went IPO and until the lockup period expires, and then the shares were yours for tax purposes. You could also now, because the lockup period expired, sell your shares to cover the full tax liability.

And then.

How Uber’s and Lyft’s IPOs Actually Worked for RSUs

Both companies changed the rules about RSUs in their IPO filings.

The second trigger was no longer “the lockup period is over.” It was “IPO Day.” When, let’s review, you are not allowed to sell your shares. Yet, all the RSUs are “released” fully on that day and you owe taxes. That day.

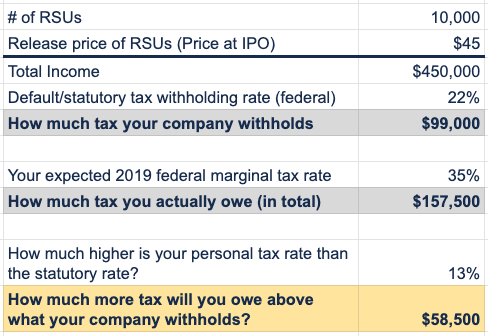

Now, companies do usually withhold the statutory 22% tax rate, usually by withholding shares from your total RSU grant. So, if you had 10,000 RSUs, you’d actually receive only 7,800.

But if you’re about to come in to a Whole Lot of Money in 2019 thanks to the IPO (or any other source of income, like a generous salary), your tax rate is waaaaay higher than that.

Let’s say your top/marginal tax rate is 35%. Sure, the company withheld 22%…but you still owe 13% on the value of those RSUs. 13% that you’re gonna have to come up with out of your own pocket because you can’t sell the shares to come up with the money. Thanks. Thanks a lot.

A chart to illustrate said craziness, for those of you so inclined. (Do note I’m talking only about federal taxes. States might want their piece, too.)

You need to pay the IRS that $58k at some point. Maybe you can delay until you file taxes next year. But in many cases, you should pay estimated taxes—in Uber’s case, it’ll be by June 15; in Lyft’s, it was April 15—so you don’t get penalized for underpayment of taxes during the year.

So, I encourage you to work with an accountant or financial planner to:

- Calculate your remaining tax liability

- Figure out whether you need to pay it now via estimated taxes or you can wait until Tax Day next year

- Figure out how to come up with the cash to pay estimated taxes, if that’s the right solution

Why This Is So Risky for You

Now, there’s a not entirely unreasonable song and dance about the benefits of doing it this way. Benefits definitely for the company and investment banks that brokered the deal, but also possibly for you, the RSU holder.

If the Uber stock price, for example, which “premiered” at $45/share on IPO day, rises to $60 by the time the lockup expires, then you will owe income taxes on $45/share instead of $60/share. Which is to say, you will owe taxes on A Smaller Amount, which means Lower Taxes…which I think we can all agree is often a good thing.

BUT, and this is where my knickers get a’twisted, by arranging it this way, the company has imposed a possibly big investment risk on you. A risk you cannot get out from under. (Well, you could by doing something more complicated like buying put options, but for “normal” people, simpler is better.)

What is this investment risk? The fact that you owe taxes on that full $45/share regardless of what the stock price does in the next 6 months. Regardless of where it ends up by the time you can actually sell it.

If the stock price ends up lower, say, $35/share, then you will have paid taxes on income of $45/share for something that, in every real way, is only worth $35/share to you.

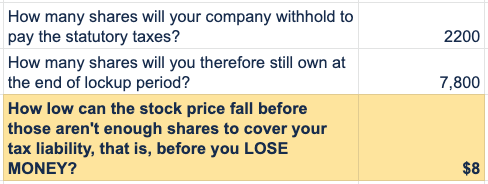

Now, you’ll still most likely end up with more money than you started with, even if the stock does fall in value. I ran a calculation for an Uber client the other day to see just how much the price of Uber stock would have to fall before her RSUs actually lost her money. Uber would have to lose a lot of value. Probably not gonna happen. But it could.

Continuing from the example above:

If Uber shares end up lower than $8 by the time this fictitious person sells her RSU shares, she will have paid more in taxes than she recoups by selling the shares.

Remember! In public companies, the nice thing about RSUs is that, as long as the company doesn’t go bankrupt or cease to exist, they’re guaranteed money! It might be more or less money, but it’s real money for you regardless of what the stock price does.

So, the idea that you could actually lose money on RSUs because of this change to the second vesting trigger…well, it sticks in my craw.

In the end, who knows what the stock price is going to do. Personally, I have my fingers crossed So Hard for my clients. This might all turn out gloriously for Lyft and Uber shareholders who had RSUs. If the stock price rises above IPO price, you will have benefited from this change to the vesting rules. And at the very least, as long as the stock price doesn’t drop below some pretty low threshold (specific to your personal tax rate), you will make some money off the RSUs.

I’m just annoyed that by changing the rules, these companies imposed a lot of unnecessary stress on their RSU holders:

- “Where am I going to come up with the extra cash to pay the full tax liability?”

- Investment risk of holding shares that you’ve been forced to pay taxes on, but that you cannot sell

So, please make sure you understand how your RSUs actually worked if you had RSUs in a company that recently went IPO. Figure out if you owe taxes now. Be aware of how much investment risk these shares are creating for you.

And if you have RSUs in a company that hasn’t yet gone IPO but intends to (<cough> lookin’ at you, AirBnB), understand how your RSUs work currently, yes, but also know that the rules can change.

Do you have RSUs in a private company (or one that recently IPOed) and now I’ve scared the bejeezus out of you? Reach out and schedule a free consultation or send us an email.

Sign up for Flow’s weekly-ish blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.