Do you want to create a smart strategy for your company’s IPO, but you have options and shares and RSUs, you don’t know how they fit together, and it all just seems irreducibly complex?

Maybe a case study will be helpful, to illustrate how one woman came up with a good solution for her specific life and equity details. My client, let’s call her Mia, has worked for a company, let’s call it FinTech, Inc., for five years. Earlier this year, it went public. Together we created a strategy that she has partly executed so far.

We abided by these priorities when creating the strategy for Mia. This is likely a healthy starting point for you, too.

- Define what this money is for in her life (i.e., define her essential goals; what does she need to feel safe, to feel fulfilled).

- Sell enough company stock to fully fund those goals.

- Minimize taxes while doing this.

- Consider keeping company stock only to the extent she doesn’t need the money for an essential goal.

To make sure you are really understanding the meaning of “priorities” here: minimizing taxes is less important than selling company stock to fund her goals. Yes, she might make some tax-inefficient decisions along the way!

Start with the Most Important Thing: What Is This Money for?

Some people already have a list of things and experiences they want to spend money on: buying a house, funding a kid’s college savings account, doing a remodel, taking a sabbatical, etc. Those people should focus on getting enough money out of company stock and into cash or a diversified portfolio ASAP, invested in a way and in an amount that is appropriate for those goals.

Clearly defined goals make this part of the game pretty easy. In my experience, it’s really easy to convince someone to sell their company stock if they get a house out of it, or a sabbatical, or something that is personally meaningful to them. Convincing them to sell their stock when they don’t have any well-defined need for it…well, it’s less convincing.

This is the situation Mia was in. She has no such clearly defined goals. She has more of a “I want to have strong finances so that I have more choice and flexibility in the future” attitude about money.

In my world, that meant selling a bunch of the company stock (not necessarily all of it, but a bunch) to put it in a robust cash emergency fund and a diversified portfolio that will be less volatile in the future than a single stock would be. Thankfully, Mia was amenable to that. She didn’t hold any strong feelings about the stock.

So, she had an overarching strategy for her work with company stock: Get enough money out of the company stock to build:

- A robust cash cushion. (This provides near-term flexibility and protection.)

- A retirement portfolio big enough to give her a robust level of financial independence. Not fully financially independent, but financially independent enough. She targeted achieving “Coast FIRE” (having a big enough retirement portfolio that she wouldn’t need to save any more to it), assuming she’d retire16 years from now. (This provides long-term flexibility and protection.)

She could assign a dollar value to each. In Mia’s case, she decided to make it:

- 1 year’s worth of expenses, in cash ($100k)

- Looking at her existing retirement portfolio, she needed an additional $700k to be Coast FIRE.

She needed $800k, after tax, out of this IPO. (Yes, these are both somewhat arbitrary targets. But also reasonable, a combination that characterizes many important financial decisions.)

Between the two, Mia will now have way more freedom to make life and career choices that aren’t motivated primarily by “how do I make a lot of money?”

If you’re doing this yourself, write these goals down and put a dollar amount next to them. It’s remarkably helpful, in my experience, to have a visually clear list of the dollar target and the “why.”

Rules of the IPO

FinTech, Inc. had a fairly standard (for the modern era) IPO setup:

- Double-trigger RSUs fully vested on IPO day.

- Employees couldn’t sell any shares until six months after IPO day (i.e., there was a six-month lockup). They could exercise options but would have to hold the shares after exercise).

- If the stock price hit certain desirable targets, there would be a mid-lockup, one-week-long trading window.

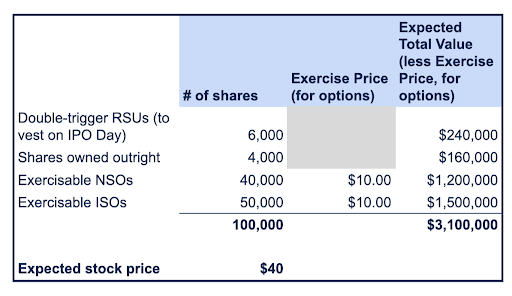

- During that limited trading window, employees could sell 25% of their total ownership as measured on IPO Day. We calculated that Mia “owned” 100,000 shares (between outright shares, vested options, and RSUs vesting on IPO day). She was therefore allowed to sell 25,000 shares.

Strategy in the Years Before the IPO

In each year leading up to the hoped-for-but-we-don’t-really-know IPO, Mia exercised some ISOs. If you have really cheap options, the upper boundary of this exercise should likely be the number of ISOs you could exercise without triggering Alternative Minimum Tax.

In Mia’s case, the exercise price was kinda pricey ($10). So, Mia chose an amount of money that she felt good losing entirely (because that’s what she risked by exercising options in a private company, especially one with no specific plans for a liquidity event), and she exercised as many options as that would buy. Turns out, that was always beneath the AMT threshold. She ended up exercising only a small fraction of her ISOs by the time the IPO rolled around.

(By the way, despite the potential tax awesomeness of exercising ISOs early, it was reasonable for Mia to exercise so few ISOs. Any money you put into exercising private-company options is money you risk losing all of. It is, in fact, entirely rational to delay exercising all options until you can also sell the resulting shares. Although it limits your upside (because your tax rate will be higher), it eliminates your downside.

Going into the IPO, she had:

Basically, she had every type of equity comp you could imagine. How should she make the best decisions across the entire suite of equity comp, not just for one type at a time?

Strategy Right Before the IPO: Choose RSU Withholding

Leading up to the IPO, Mia had one big decision to make: When her RSUs vested on IPO day, she could default into the statutory 22% withholding rate for federal income taxes on the RSU value, or she could choose to withhold 37%.

Even though Mia didn’t have much in the way of RSU shares—which meant that this choice didn’t involve a lot of dollars—she chose to have 37% withheld. Why?

- This reduced her “concentration risk” sooner. We had no idea what was going to happen to the stock price before she’d be able to sell any shares. If the stock listed at $50 and dropped to $20, she would have effectively “sold” at that higher $50. Yay! Even if the stock price ended up increasing, she at least didn’t have to worry about it in the meantime.

- Even though her RSU income wasn’t going to be big this year (meriting the highest tax-bracket withholding), she had plans for exercising NSOs, and that would make her income high (and therefore tax rate high) this year.

Strategy During the Lockup and Right After: Turn Company Stock into Cash ASAP

After IPO Day, when the rules were in place and we had some sense of the stock price after the company went public, that’s when most of the strategery could usefully happen.

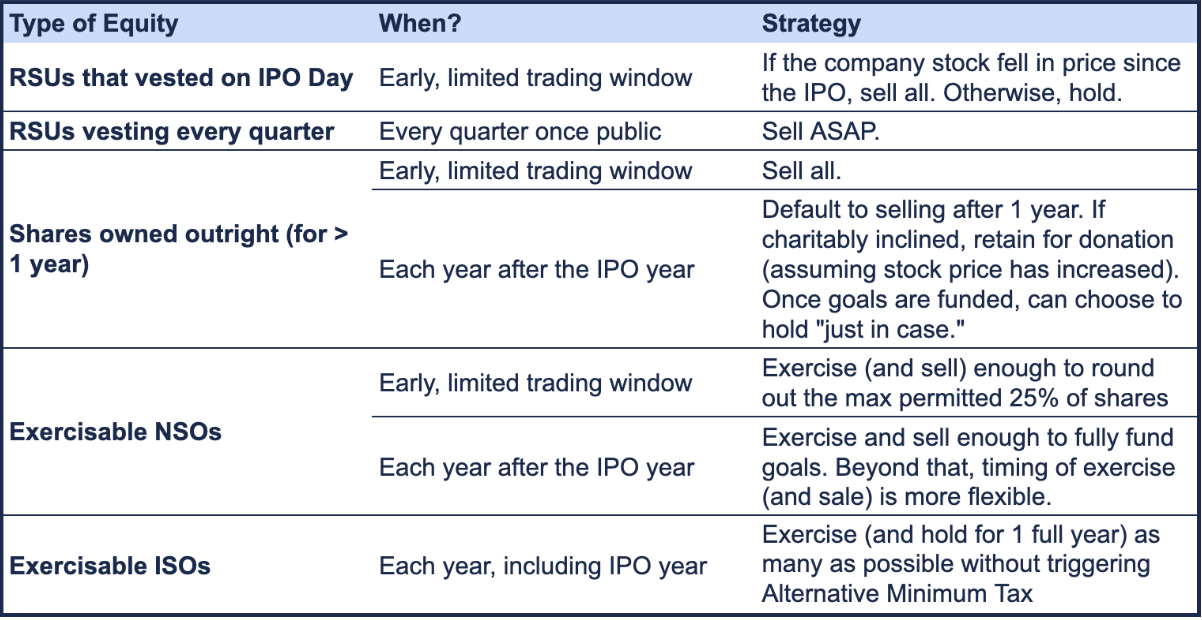

RSUs that Vested on IPO Day

When the special, limited trading window opened up in the middle of lockup, she wanted to diversify (start selling).

Because Mia’s RSUs were “double trigger,” (which is the norm for private-company RSUs), all of Mia’s 6000 time-vested RSUs had fully vested on IPO Day. Almost 50% of the RSUs were withheld (between state income tax and 37% federal tax), so Mia then owned 3000 shares from that vesting.

Leading up to the limited trading window, she didn’t know exactly what she was going to do with those shares. We made this plan:

- If the company stock rose in price since the IPO, she’d keep it, so she wouldn’t pay the higher short-term capital gains tax on that gain, as she’d only held the shares for a few months. We’d have to sell more of other kinds of shares to fill that 25,000.

- If the company stock fell in price since the IPO, we’d sell it. She wouldn’t incur any tax bill (although wash sales would likely mean she couldn’t benefit from that tax loss until future years). This would mean we’d sell fewer of the other kinds of shares to fill that 25,000.

As it turns out, the stock price fell from IPO to limited trading window. It had IPOed at $40 and was down to $30, so she sold those 3000 shares she had from IPO Day RSU vesting. These ended up being the tax-wise cheapest shares to sell…because she sold them at a loss.

She had now sold 3000 of the permitted 25,000 shares.

Shares She Already Owned

Mia owned 4000 shares of company stock. She sold them all during the limited trading window.

Because Mia had already owned these shares for at least one year, she would get the lower, long-term capital gains tax rate when she sold them. These were the second cheapest shares tax-wise to sell.

Had Mia had significant charitable intentions, she might have kept these shares to donate (instead of cash), because that’s tax awesomeness.

One thing that didn’t apply to Mia but might to you: If you acquired the stock early enough in the company’s timeline, it might be Qualified Small Business Stock (QSBS), which would eliminate most or even all federal capital gains tax on the gain when you sell. So, before you sell, make sure you know the stock’s QSBS status!

She had now sold 7000 of the permitted 25,000 shares.

Exercisable NSOs

To sell the remaining 18,000 of the permitted 25,000 shares, she looked to her NSOs. Because you owe income tax (on the “spread” between exercise price and fair market value) the moment you exercise, it costs a lot of money to exercise 18,000 NSOs ($10 x 18,000; plus taxes on the spread). But because she sold at the same time (and she could set aside some of the cash proceeds to pay the taxes), Mia didn’t put any of her existing wealth at risk.

You should know that there is no good reason to exercise and hold NSOs (in a public company). So, when Mia exercised, it was assumed that she would also sell. Read my favorite blog post on this topic.

We also took into consideration the idea of the “leverage” her options provided (leverage = exercise price / fair market value). NSO leverage isn’t a particularly intuitive concept (at least, not to me!) but it boils down to this: It would be silly to exercise the options at $10 if the fair market value were only $11. You only get, in a sense, $1 of value. That leverage is high ($10/$11 = 91%). It’s better to wait until you get more bang for your exercise buck.

During the trading window, however, the stock price was $30, so leverage was 33% ($10/$30). Leverage below 40% makes it worthwhile, as a rule of thumb.

RSUs as They Vest, Now in a Public Company

One of the challenging transitions when your company goes from private to public is how your RSUs work. When your company is private, usually you have no control over RSUs and do nothing. It is just Future Fantasy Money. Once your company is public, when those RSUs reach their vesting date…

- They immediately turn into stock.

- They are treated as taxable income.

- You can sell them for actual dollars.

- You probably don’t have enough taxes withheld on the vest and will therefore end up with surprise tax bills.

The best practice for RSUs, in public companies, after they vest is: Sell ASAP. And this is what Mia is doing. Remember, there is no tax benefit to holding RSU shares after they vest. No really.

Remember, as long as Mia remains an employee, she will continue to get new stock via RSUs vesting. So, whatever the fate of the company stock, she will share in it via the value of those RSUs upon vest, even if she were to sell all the rest of her stock.

Exercisable ISOs

I consider ISOs the most complicated of equity comp types, so I leave it for last, both in this blog post, and in Mia’s strategy in general.

ISOs have this awesome tax treatment of not incurring tax at exercise as long as you stay under the Alternative Minimum Tax threshold. (Remember that this is in contrast to exercising NSOs; tax is always due when you exercise NSOs.) Also, as long as you hold the stock for at least a year after exercise, you’ll get the lower long-term capital gains tax rate on the gain when you eventually sell.

Add on top: That AMT threshold, in general, goes up the higher your ordinary income is. So, with the RSUs that vested at IPO and continue to vest every quarter now that the company is public, and especially with the exercise of NSOs, she now has a very high ordinary income this year.

What does that mean for Mia’s ISO strategy? It allows her to exercise (and hold…to get the tax benefits) a bunch of ISOs with no tax bill.

How many? Welp, this is where she brought in her CPA and asked them to model how many ISOs Mia can exercise without triggering AMT. Thank you, CPAs with equity-comp expertise and a service model that includes an annual tax projection!

I still advised Mia to only exercise as many ISOs this year as she could without triggering AMT. Why?

- She doesn’t plan to leave the company in the near future, so she should have future years in which to continue to exercise the ISOs. (After you leave a company, your ISOs might outright expire. But if they don’t, they will convert, by law, to NSOs after 90 days.)

- This keeps her risk of losing money with the company stock lower. Sure, she’s putting that exercise-price money at risk, but she’s not also putting tax money at risk.

Yes, this will add to her collection of company stock (in conflict with our general goal of reducing the concentration). She is knowingly increasing concentration risk because the possible tax benefits are so good. By itself, that likely wouldn’t be enough, but this is only one part of a larger strategy of sell, sell, sell.

I find this bit of mental accounting helpful: Mia isn’t putting any of her existing wealth at risk. The money she’s risking by exercising and holding ISOs is money she got from selling other FinTech, Inc. stock.

[Side note: AMT is not to be avoided at all costs under all circumstances. There are situations in which exercising a bunch of ISOs and triggering AMT is a reasonable choice. If you pay AMT this year, you get an AMT credit and it’s possible to get that credit back in future years. That said, it still puts you at higher risk of loss. You’re spending more money to buy stock…whose price might then drop.]

Strategy in 2026 and Beyond: She Can Be a Bit More Nuanced

Remember our high-level strategy:

Priority #1 = Sell enough stock to fund goals.

Priority #2 = Minimize taxes.

What does this prioritization look like in practice? In Year 1, sell sell sell. In Years 2+, once she has funded her goals from those Year 1 sales, she can choose to slow down the sales and let tax considerations (or risk-taking) drive the bus more often.

What will she do with her RSUs? Mia will continue to sell them as they vest in 2026 and beyond, as long as she stays at FinTech, Inc. Because, to repeat the message, there is no tax advantage in holding on to RSUs after they vest.

What will she do with the shares from exercised ISOs? These are only shares she will hold. She’s going to hang on to them for a full year (to get the lower tax rate on the gains) and then sell. If Mia develops a charitable plan in the meantime, these ISO shares (assuming the fair market value is higher than their $10 cost basis) will likely be the things she should donate to charity, not cash.

What will she do with her exercisable options? Each year she starts the NSO/ISO dance again:

- She exercises (and sells) some NSOs (as long as leverage < 40%).

- If she wants to prioritize taxes over diversification, she could reduce the number of NSOs she exercises in order to keep her income below a certain tax rate. (Her CPA can help her calculate just how many NSOs that is.)

- Then she sees how many ISOs she can exercise (and hold) without triggering AMT.

She now has much more flexibility in how she treats company stock:

- Keep more: If she has an emotional connection to the stock, or doesn’t want to sell everything because “what if?!”, then cool, let’s leave more NSOs unexercised or let’s keep some exercised ISO shares past the one-year date.

- Keep less/none: Statistically speaking, any concentration in a single stock increases your risk without a concomitant increase in your reward. 100% diversification (i.e., getting out of all of her stock) is her best chance of having successful long-term investing. This, by the way, is where I stand. But I don’t impose this perspective on clients when their life goals don’t require it.

There’s more detail to the “2026 and beyond” strategy, but I’m keeping things short and simple here for the sake of digestibility.

Here’s a summary of Mia’s strategy by type of equity:

Feeling overwhelmed? I’m not surprised.

Have a better sense that all these pieces can and should fit together? I hope so.

Convinced of the primary importance of clarifying what this money is for in your life, and of orienting all your decisions around supporting that? Good.

If you want to work with a financial planner who can help guide you through your IPO in a way that feels right and true, reach out. Even if I can’t help you myself, I Know People.