As so many of my blog posts seem to, this one starts with “Congratulations! Your company is going IPO! Now you have…all these decisions to make.”

And one of those decisions, which you have to make before you have any clue how well the company stock is going to do, is:

Do you want to withhold 22% or 37% of your RSU shares for federal taxes when they vest on IPO Day?

In already-public companies, I’ve never seen a company do anything other than the statutory 22% withholding when RSUs vest. Which means that once your company is public, you’ll need to stay on top of your tax bill throughout the year because you’ll need to pay additional taxes on RSU income. (See below re: hiring a CPA.) [Updated 5/15/2025: Many big tech companies have since moved to allowing their employees to withhold more than 22% on RSU vests, which has made people’s taxes much easier to manage.]

So, it is nice that companies offer you that choice for the RSUs vesting on IPO Day. Sometimes 37% (the highest income tax rate) can be very handy, and 22% is too low for many people who work in tech.

Here are the two challenges of this decision, as I see it:

- 22% is too low. 37% is too high. (For most people.) But you can’t choose an in-between.

- Withholding for taxes is like selling the shares. And you’ll be “selling” those shares at the IPO list price. But you don’t know what that “sale” price will be at the time you have to make the decision to “sell” (withhold)! And you don’t know whether the price will go up or down after IPO! Stressful.

22% is too low. What would I still owe?

First thing, then, is to figure out what your tax liability (probably) will be…as it’ll likely be higher than 22% and lower than 37%.

You’ll need to guess at the value of your RSU shares when they vest. You can even run the calculation at a few different prices to get a sense of possibilities.

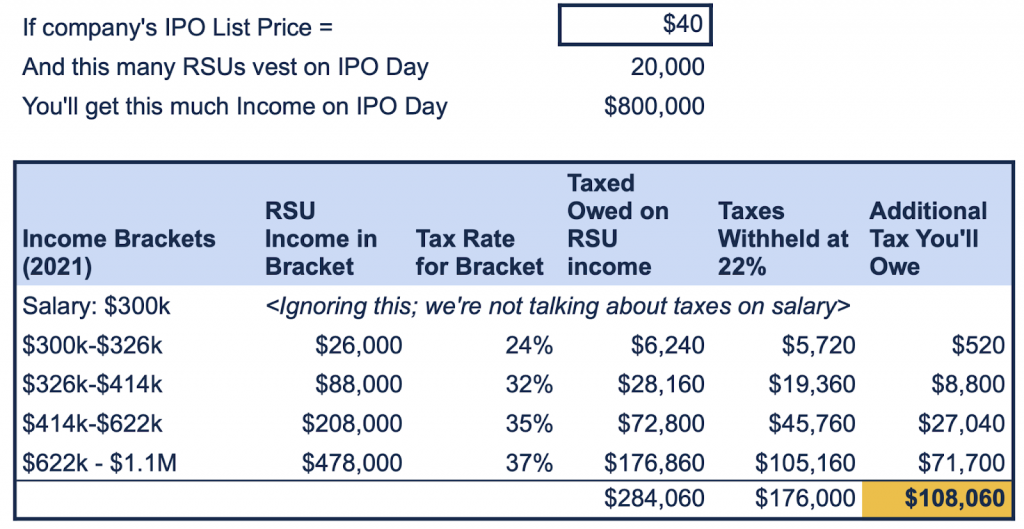

In this example, you have a salary income of $300,000. On top of that, you’re getting RSU income on IPO Day. We guess that the stock will list at $40. Maybe that’s the rumors floating around. Maybe that’s the latest 409(a). Maybe it’s the last price the stock sold at on the private secondary markets (like ForgeGlobal and EquityZen).

Really, it’s a guess. (Many of my clients guessed Airbnb was going to IPO at around $38, which was the most recent valuation. It listed at $68. Whoops!)

If you withhold only 22%, you will have (roughly…the above calculations aren’t to be relied upon for your specific tax situation!) $108k more to pay in taxes on your RSU income.

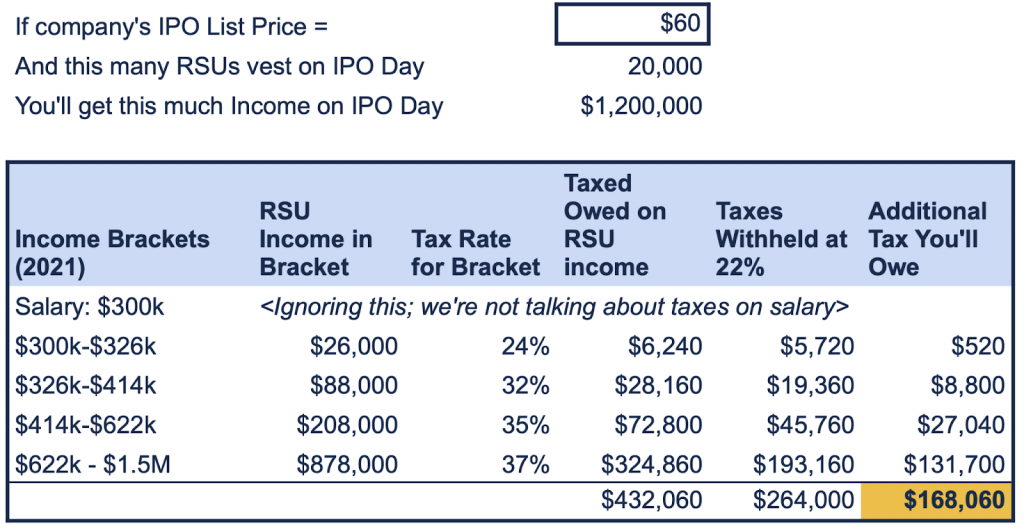

Let’s say it instead lists at $60.

Now you would owe an extra $168k in taxes. And maybe even owe them by the next estimated taxes date (January 15, April 15, June 15, September 15).

Now the question becomes:

If you withhold only 22%, how will you pay the remaining tax liability?

That $108k (or $168k)?

Maybe you have stockpiled some cash.

Maybe your company is going to give you a trading window right after IPO so you can sell more stock to cover that tax liability. (Very recently, companies like Airbnb, Doordash, and Robinhood have allowed this. But this is a very recent development! Employees at companies like Uber had to wait the entire 6-month lockup period before being able to sell. And it worked out poorly for them.)

Maybe you have some other income coming up that could cover the tax liability.

In any case, you really should know how you’re going to cover it, especially if it’s a big liability!

On the other hand, 37% is too high.

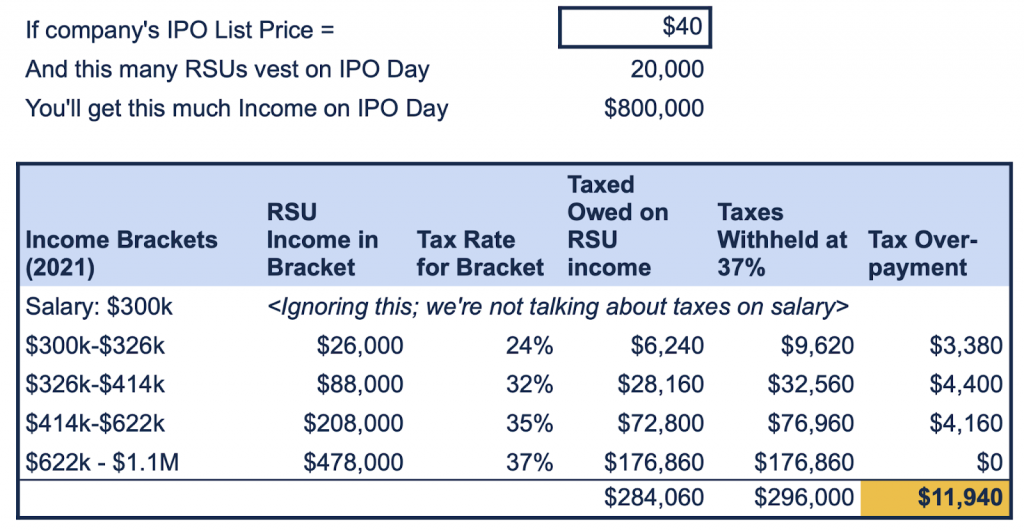

If you withhold 37% instead, you will likely withhold more shares than you need to in order to fully pay the taxes due.

Back to that “IPO lists at $40/share” example: you can see how you’ll be overpaying your taxes. (Notably, the overpayment isn’t as great as the 22% underpayment was.)

Why would you withhold 22%?

So, now that you maybe kinda sorta understand the math implications, how do you make the decision?

Because the correct answer is based on your personal situation (both objective and emotional) and on totally unknowable things like the IPO list price and the future performance of the stock, here are some things that might make 22% withholding the better choice:

- You think that the stock price is going to go up after listing (a price “pop,” as happened with Airbnb), and you want more shares left over after withholding to benefit from that rise in price. And (and!) you wouldn’t be devastated—emotionally or financially—if the price actually dropped after listing.

- You will feel…okay if you withhold at 22% and the price instead falls.

- If the price falls, and you have to sell at a lower price to pay taxes, this won’t compromise your ability to use this money for something else that’s important to you.

- You have other, reliable ways of paying the remaining tax liability.

- You have an opportunity immediately following IPO to sell more of your shares to cover the remaining tax liability (an initial trading window like the ones Airbnb and Robinhood offered).

Why would you withhold 37%?

- You fear the stock price might go down after listing (as happened with Uber, and so far with Robinhood).

- You will feel…okay if you withhold at 37% and the price instead goes up.

- You want to diversify more quickly out of a heavy concentration in your company stock. (Always a financial planner’s dream; we are a conservative and, well, statistically minded lot.)

- You don’t want a tax bill hanging over your head.

- You have an opportunity right after IPO to sell more of your shares…and you want all of that money going towards a short-term goal you have (home downpayment?) instead of needing to be set aside as tax payment.

- You will continue to get more company stock (ESPPs, RSUs vesting, exercising options) as long as you remain at the company. Even if you withhold “too much” on IPO day and the price goes up, this future stock can all benefit from that higher price.

Recent IPOs: Would 22% or 37% Have Been Better?

Airbnb went IPO on December 9, 2021. Some of our clients had 22% withheld. Some 37%.

Airbnb listed at $68. Which means those shares got withheld for taxes (effectively, sold at) $68/share.

Then the price popped to $150. Had we known, it generally would have been better to withhold the lower 22% and then sell the permitted 15% of shares in the first 7 days at a price at least 2x what the list price was.

And yes, there was some gnashing of teeth among some of the clients who had chosen to withhold 37%.

But hindsight is a b*tch. Part of our consideration in making that decision is that it didn’t have to go that way. The price could have fallen from the IPO list price.

Enter Robinhood.

Robinhood just went IPO on July 28. It, too, offered its employees the choice between 22% and 37% withholding on their RSUs vesting on Day 1.

Robinhood listed at $38. And then immediately lost 12%, ending up closing the first day of trading at $34.

As of the time I’m writing this blog, the initial IPO trading window isn’t yet over and the stock price might yet soar (anything can happen). That said, I suspect that people who withheld 37% (at that higher $38 list price) are probably feeling pretty good about their choice right now.

Even worse, can you imagine having withheld only 22% of Blue Apron stock, if 37% was available (I don’t know)…and then this is the stock performance since then?

Please work with a CPA.

Thought I’d throw this in here. Again. As I almost always do when I talk about equity compensation. This decision is a great example where CPAs can help you understand what your tax liability could be, ahead of time, and what it is, after the fact.

Working with a CPA is helpful in the 22% vs 37% discussion, but also helpful going forward, as now your RSUs will be Worth Money when they vest in your now-public company, and you will likely owe more taxes on them above what’s withheld.

Whatever your decision, Congratulations! We’re talkin’ Money, Baby! And good luck! IPOs are super stressful!

Disclaimer: This information is for educational purposes only and should not be misconstrued as tax advice. Flow Financial Planning is not an accounting firm, and does not provide accounting services. Please see an accountant for advice specific to your situation.

Do you want to work with someone who can help you make all these impossible decisions when your company goes public? Schedule a free consultation or send us an email.

Sign up for Flow’s weekly-ish blog email to stay on top of my blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Meg Bartelt, and all rights are reserved. Read the full Disclaimer.