How long have you been paying attention to your investments, or to the stock market? Has it been only for the last few years, or, maybe only since 2009?

2009, by the way, is otherwise known as the bottom of the market during the Great Recession. Also otherwise known as the beginning of one of the greatest bull markets (that is, markets that go up) in US stock market history.

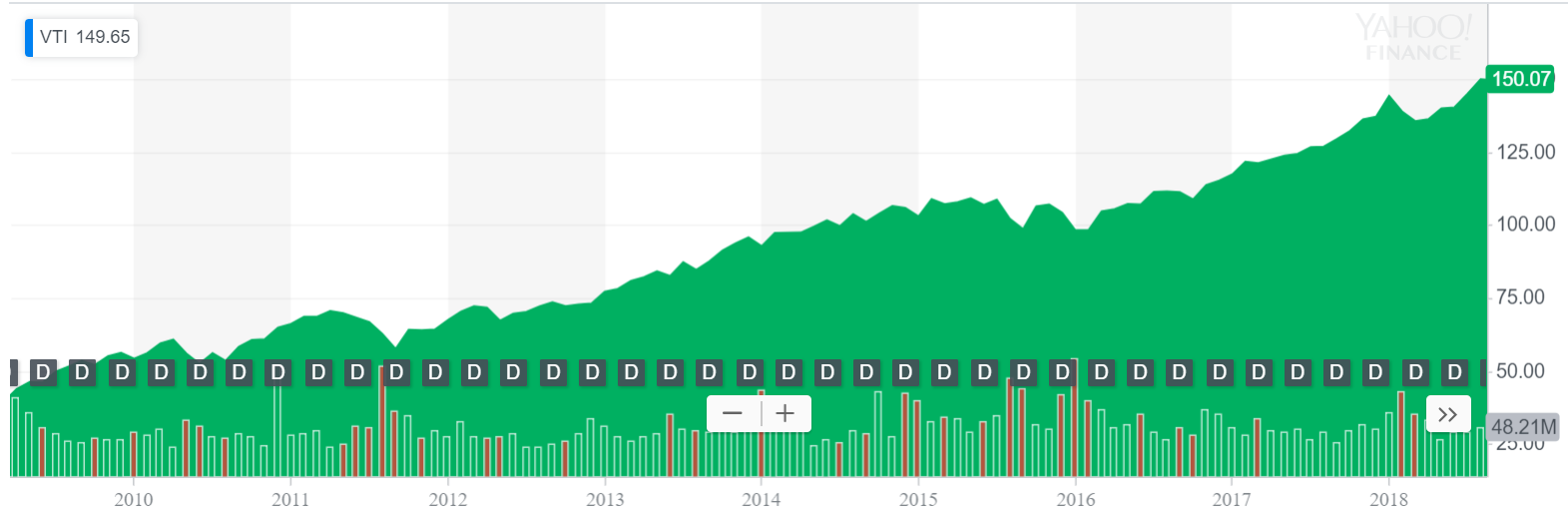

And if you have only tuned in to investing and the stock market in the last few years, this is the kind of result you’re accustomed to:

(Source: https://finance.yahoo.com)

Look at that lovely, pretty uninterrupted upwards trajectory! (Green thrown in just for emotional manipulation.) This is the performance of Vanguard’s Total Stock Market Index fund, a good representation of “the general stock market.”

It’s understandable, then, if you’ve felt pretty sanguine, pretty comfortable with the whole investing thing. After all, it only ever really goes up, right?

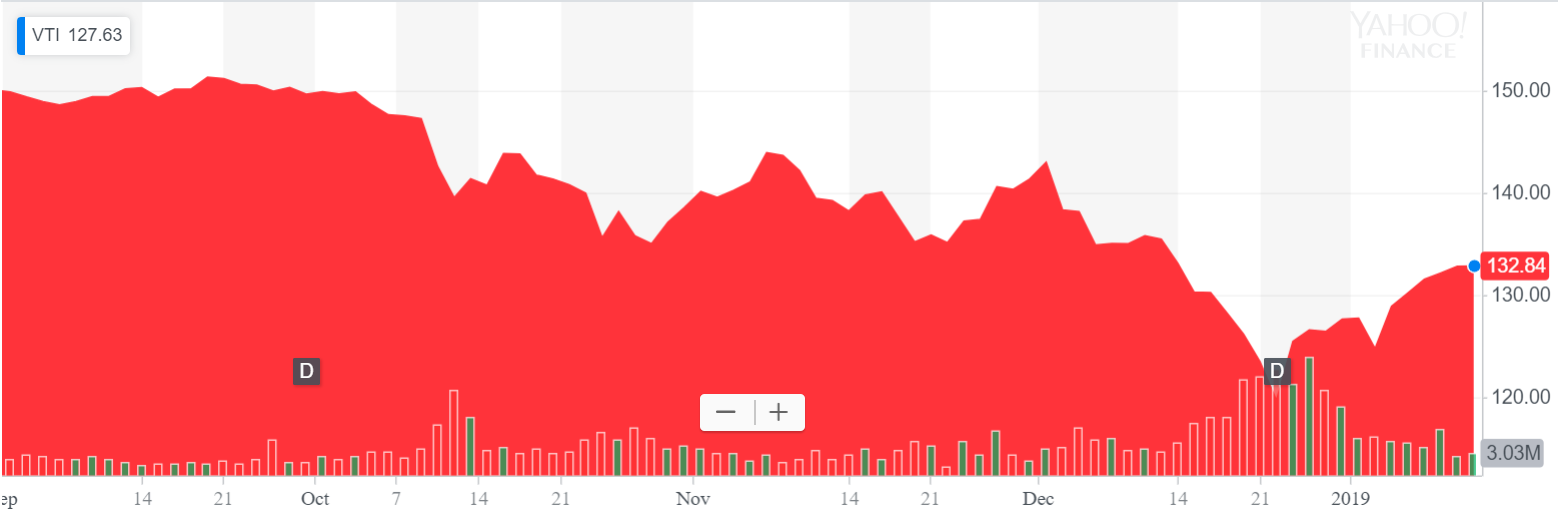

And then, in the last few months of 2018, we all got a rather unpleasant surprise:

How are you even supposed to react to this unpleasant and very unusual (at least, for the last 10 years) change of fortunes?

Your 401(k) Has Betrayed You

Most of my clients have 401(k)s that they’ve been blindly saving to for years now. (When I say “blindly,” I don’t mean that in a negative way…I actually think it’s very very good to simply shovel money into your various savings buckets without it being a big thing.)

It’s been reeeeall easy to get my clients to follow my advice to continue to max out their 401(k)s (or even more, if they can make after-tax contributions) and invest in target-date retirement funds, which are heavily invested in stocks if your retirement date is decades out.

Why has it been so easy? Well, first reason is my superior persuasion skills. Obvs. Second is that it’s comfortable to invest in stocks when stocks Only Go Up.

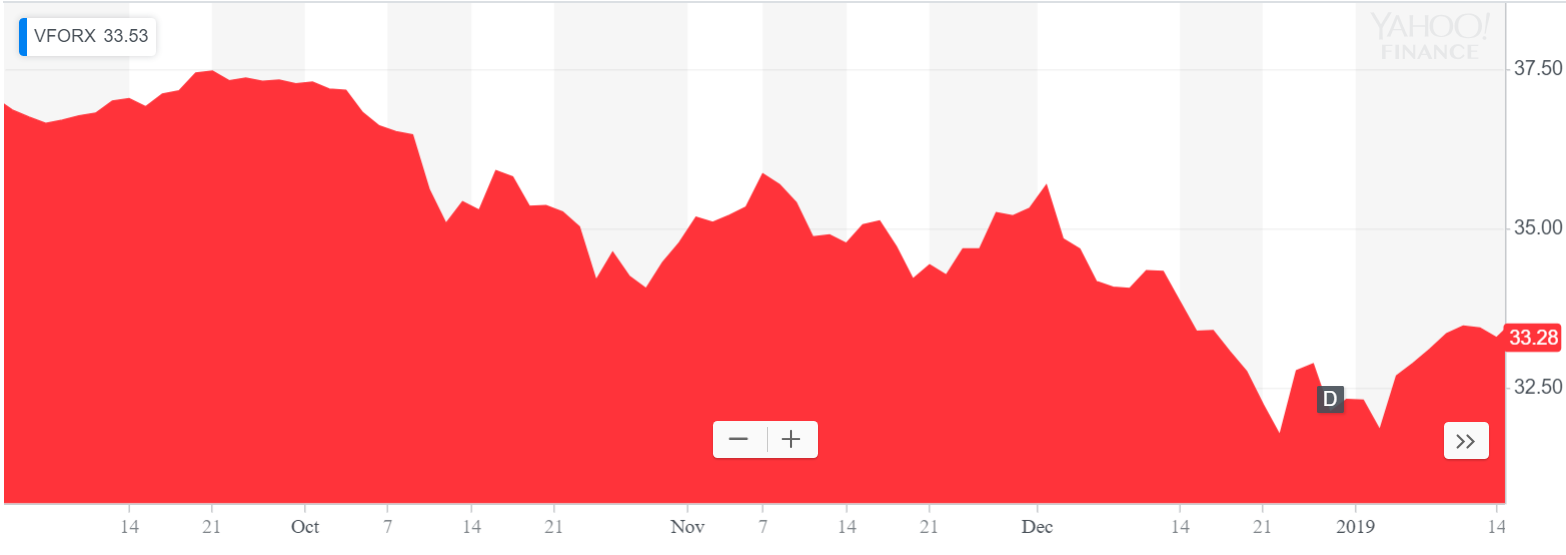

But let’s take the Vanguard Target Retirement 2040 fund as an example. From early September to early January, it looked like this:

Damn you, 401(k)! Why hast thou forsaken me?!

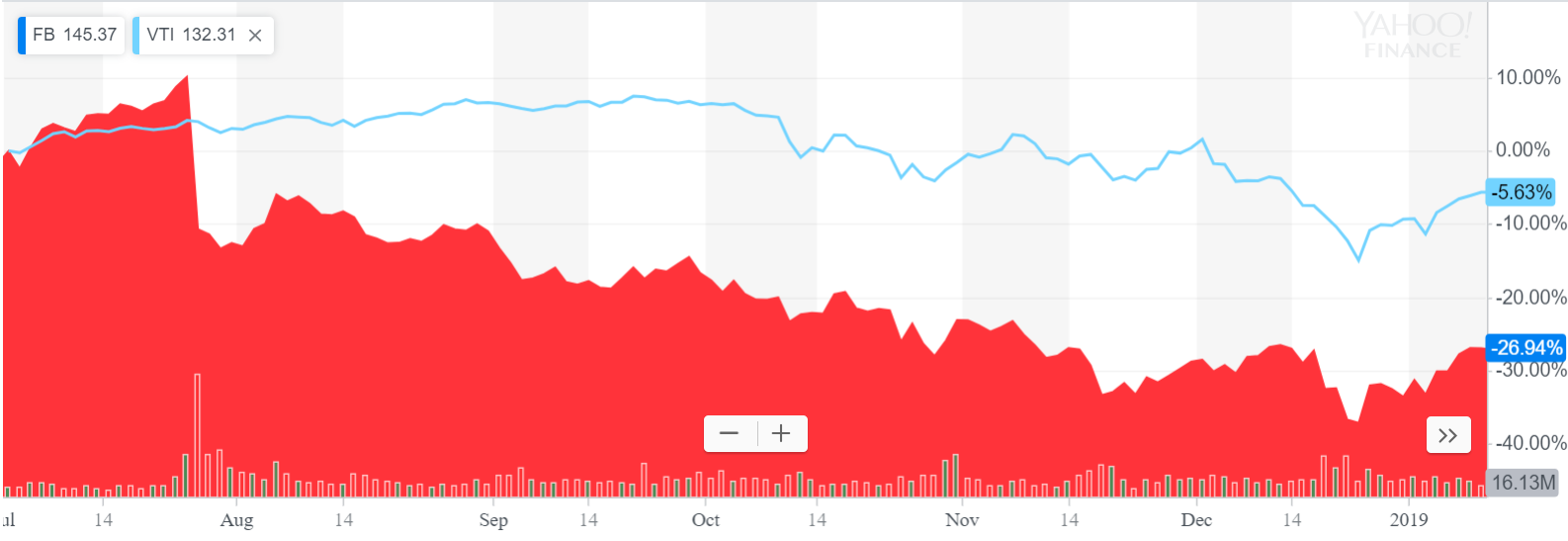

How’s Your Company Stock Faring?

Even if your 401(k) has been a bit disappointing of late, maybe your company stock has been a shining beacon of investment awesomeness. Orrrr, of course, it might be making things even worse for you.

My clients at Facebook certainly had a rather crappy second half of 2018 (compared to the general US stock market, in the blue line):

If you’ve got Facebook stock, you could probably be easily persuaded by my typical advice to clients who own company stock: “sell most of your company stock ASAP.”

But my clients holding Etsy stock in the 2nd half of the year:

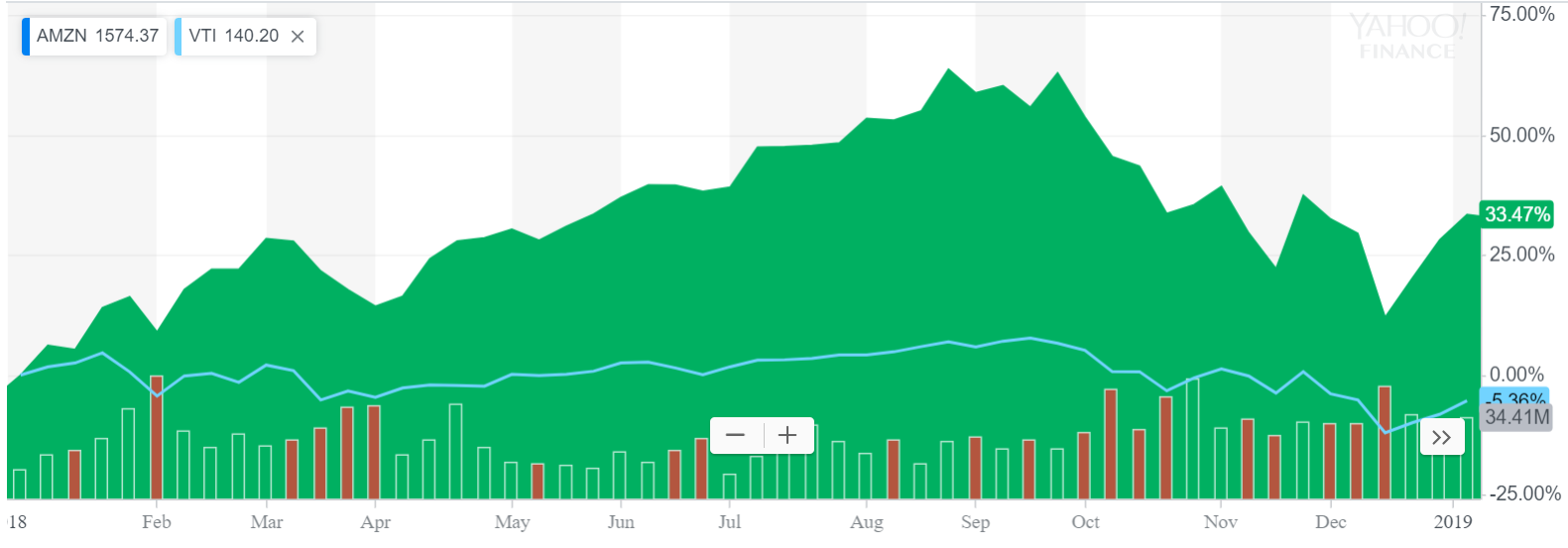

or Amazon stock for all of 2018:

…are feeling Pretty Smug right now. And also perhaps questioning my judgment: “You want me to sell my company stock? But, but…it’s kicking butt!”

So, it turns out that some tech companies and their stock are cushioning the investment blow for some of my clients and maybe for you, too. It might therefore be confusing the matter of “How should I approach my investments?”

(To be clear, I’m Very Happy for my clients who had, for whatever reason, large holdings in Amazon or Etsy or Twilio, etc. during 2018.)

But what I’d love for you to take away from this (and what I hope my clients do, too) is that

This changes nothing about how you should treat your company stock.

Holding company stock is incredibly risky:

- Concentrated holdings in any single stock is risky, as you can’t smear your risk out over a bunch of companies, some of which might go up, some of which might go down. If your company stock goes down, ain’t nothin’ offsetting that fall.

- Concentrated holdings in the same company that pays you your salary (and possibly that affects the value of your home, as might be the case if you live in Seattle and work for Amazon) is extra de-duperty risky, as any faltering in company performance might simultaneously pummel your investment portfolio, the value of your home, and your ability to earn money.

So, you need to think about how holding company stock will affect your finances and your life. Sometimes it’s perfectly fine to hold significant amounts of company stock…as long as you understand what can happen. That is, that you can lose much, most, or all of that money…and are you okay with how that will affect your finances and your life?

The fact that some tech-company stocks have done particularly well or particularly poorly in the last year doesn’t affect that fact or that strategy at all.

[Note: Now, I know I’m committing felony-level #chartcrimes here by having different time frames for most of these charts. I simply want to illustrate the perspective that many of my clients (and many of you!) might have on your company stock versus the stock market in general.]

What You Should Do at This Point

You’ve probably read all the Very Reasonable and Prudent advice about “Don’t do anything. Don’t wig out and sell all your stock. Don’t go to cash.” So, I won’t belabor that point because, well, it’s been thoroughly belabored already.

What I’d like to present to you is simply a different perspective on the losses in the stock market. And hopefully that new perspective will encourage the right behavior. Now, I didn’t come up with this perspective, it’s just one of my favorite ones.

After the stock market falls in value, it’s as if stocks are on sale. It’s the best time to buy.

A share of Vanguard’s Total Stock Market Index Fund, for example, cost about $149 in early September. Now it costs (as of January 14, 2019) about $132. It’s as if it’s been marked down by 11%.

You’d rather buy a shirt when it’s on sale, right? So, you’re better off buying stocks when they’re on sale. You get the very same thing, but at a lower price. If you were buying stocks in September (and, if you have a 401(k), you almost certainly were), why oh why would you stop buying them now, when they’re cheaper?

So, to keep it short and sweet:

Keep saving and investing in your 401(k) and other investment accounts, just as you were 6 months ago or a year ago.

There are some things you can do to “optimize” your investments:

- You can “rebalance.” If you’re in a target-date retirement fund, surprise! You’re already rebalancing. Those funds do it automatically for you.

- You can intentionally sell investments at a loss to reduce your taxes, a.k.a. “tax-loss harvesting.”

Keep in mind, though, that tactics such as these are simply a thin layer of icing on the Cook’s Illustrated Sour Cream Chocolate Bundt Cake of continuing to save and invest and otherwise not touching your investing. Also, I must note, that while the stock market has fallen in value, it has had far larger losses in the past, so you’ll eventually have to deal with one of those “far larger losses” yourself.

As I finish this writing this, Jack Bogle has just died. The founder of Vanguard. The creator of the first index fund. And a man with a mission to improve the financial industry for regular investors, like you and me. His last book was called Stay the Course, and that is the simple, if not easy, message I leave you with here.

Is your first true taste of stock market losses making you think that maybe working with a financial professional is a good idea? Reach out to me at or schedule a free consultation.

Sign up for Flow’s weekly-ish blog email to stay on top of my blog posts and videos, and also receive our guide How to Start a New Job (and Impress Yourself and Everyone Else) for free!

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Meg Bartelt, and all rights are reserved. Read the full Disclaimer.