Airbnb is going public. You have a bunch of RSUs. You are wide-eyed with uncertainty and excitement. Discuss.

What’s Important to You?

The very first blog post in this series about Airbnb going public emphasized, above all else,

What’s the first thing you should do? It’s the first part of any good financial plan: Get clearer on what you want in your life.

I know you already know this. Everyone’s listened to Simon Sinek for goodness sake. But it’s so easy to lose sight of, amirite? So let me put it in your face once again.

The answer to this question will make it way easier for you to figure out what to do with your RSUs.

I suspect many of you out there really want to be able to:

- Feel safer (in financial planner parlance, we call that “an emergency fund” or the closely related “I’ve had enough of this sh*t” fund)

- Buy a home

- Pay off debt

- Retire early or at least have more independence

- Help others

- Start a company

- Whatever else sets your heart atwitter when you think about actually having it in your life

How necessary are these things for you to live your ideal life? A fulfilled life? If the answer is “Very!” then that is what the Airbnb money is for. Not to sit there in stock form, maybe losing value, maybe gaining value, but most certainly not getting you closer to your ideal life Right Now.

On the other hand, to the extent that you already have what you need in life to feel fulfilled, then you can think more about keeping the Airbnb stock. If it’s just icing, then we care less about whether the stock gains or loses value. If you need that money to have the cake, then why are you risking it?

How Your RSUs Will Work When Airbnb Goes Public

As a private company, Airbnb RSUs have a “double trigger” vesting: they don’t turn into actual company stock for you until two things happen:

Requirement #1 = a service-based requirement. Which is to say, you stay at the company long enough to pass vesting dates. In public companies, this is usually the only vesting requirement. (And after Airbnb goes public, your not-yet-vested RSUs will require only this.)

Requirement #2 = Some liquidity event. In this case, going public! If you’ve been at Airbnb for at least a year, some of your RSUs have already passed Requirement #1. You’re just waiting for the IPO or direct listing.

Well, now yer gettin’ that IPO or direct listing. (As of the writing of this blog post, we don’t yet know for sure what the company is going to do. From here on out, I’m just going to refer to an “IPO” because it’s easier.)

Our first question is: What specific day around going public is Requirement #2 met and will your RSUs fully vest (become income)? Is it the very day it goes public? Is it the day the lockup period—which is usually six months long after an IPO, and maybe 0 days for a direct listing—expires?

It looks to me as if the most likely timing for your RSUs to fully vest will be in early 2021. (Don’t know how much detail is appropriate for me to put in a public blog, so I’ll keep it vague.)

So, our next question is: What will you be able to do with the stock after the RSUs vest? Will you be in the middle of a lockup period? Will you have to continue holding them, hoping they don’t lose value? Or will the lockup period be over by then, and you could sell them immediately?

Uber’s IPO is a cautionary tale of Airbnb RSU holders. Uber’s RSUs vested on IPO Day, and Uber people had to wait six months to sell them…while watching the stock price fall from $45 to around $30. But they owed taxes on a $45 stock value. Ugh. I wrote up the sad tale of how this mismatch in timing sucked for Uber RSU holders, and the logic still applies to Airbnb. And in fact, it was just announced that current and former Uber employees are suing Uber over this very issue.

Should You Sell, Keep, or Donate Your RSU Stock?

Most likely, you should simply sell your RSUs.

How can I make such a blanket statement? ‘Cause I put the words “most likely” in the front.

My general advice (note the presence of “general” and absence of “personal”):

Sell at least enough RSUs as soon as you can to cover the tax bill for the RSUs.

This way, at the very least, you will not lose money on the RSUs, if the stock price falls. Crazy to think of, but yes, you can lose money on RSUs because stock prices can fall. (I probably don’t have to tell you that, if you’ve been obsessively watching Airbnb’s 409(a) over the last 9 months.)

The Risk of Having Too Much Airbnb Stock

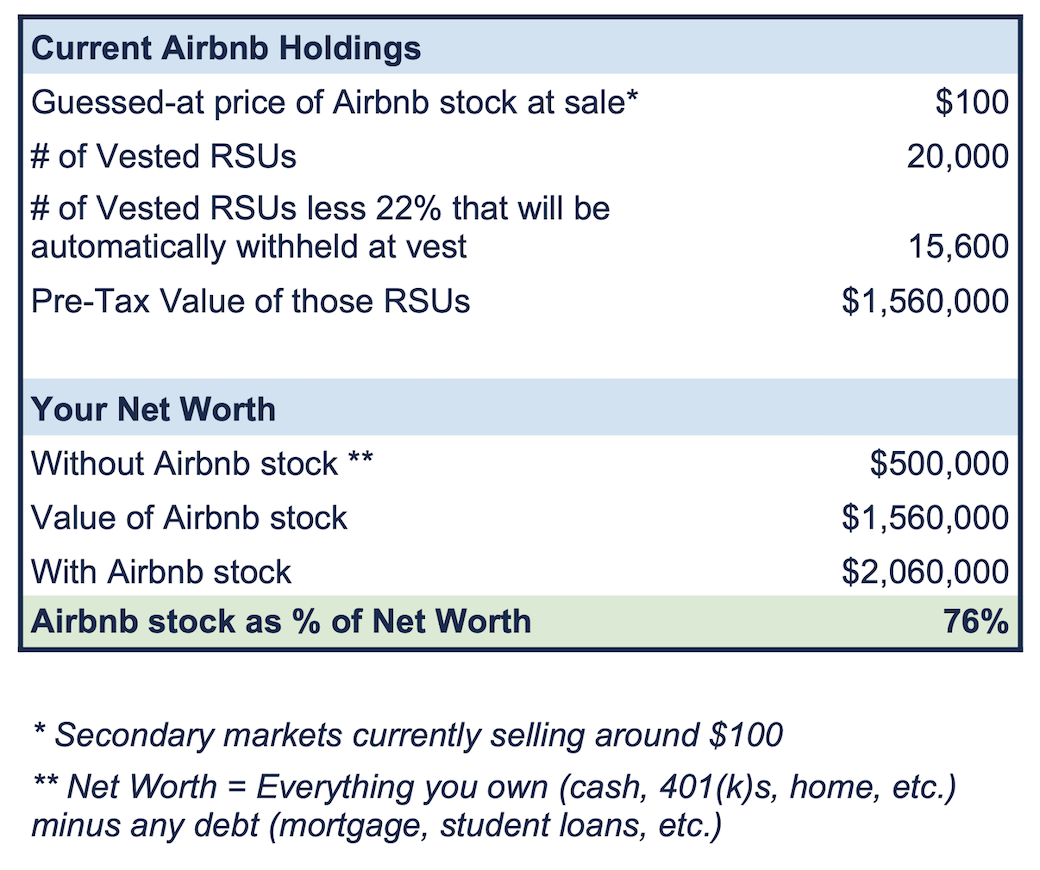

How much of your wealth is tied up in Airbnb stock? The higher it is, the more risk you take on.

This is a basic tenet of investing: diversification lowers risk, concentration (in this case, in Airbnb stock) raises risk.

How can you figure this out? I find inadequacies with every way of doing it, but I think a reasonable way to calculate it is this:

In the conservative financial planning world, we prefer to have at most 5% of your wealth tied up in a single investment. I’m guessing for most of you, Airbnb represents waaaaay more than 5%. The above example of 76% is probably a lot closer to your situation.

Which means that your financial fate is strongly linked to Airbnb’s. This one company can make or break your finances. What happens if Airbnb stock loses half in the year following the IPO? How much wealth would you lose? Calculate the number. What is your gut saying?

Now, if we come back to our first point of discussion: What’s important to you? What would you use this money for?

If you need this money to accomplish important things, then you really shouldn’t be taking the risk of keeping your money so wrapped up in this one stock. And you should focus on selling, locking in those gains.

If you don’t need this money to achieve your ideal life, then there are actually two opposite ways of thinking about what you should do with your Airbnb stock:

- You can “afford” to keep your wealth wrapped up in Airbnb stock, because if it loses value, who cares. You already have the life you want.

- You’ve already won (you have the life you want), so stop playing the game. Just sell out Airbnb stock, lock in the gains from your years of employment there, and be done with it.

If You Are Still an Employee, with More RSUs Vesting in the Future

This advice goes for any public-company employee with RSUs:

Sometimes it’s emotionally hard to sell RSUs as they vest because the stock could gain in value after you sell, and then, boy, you’d feel dumb.

Here’s one thing I always bring up with my clients: Look at your future RSU vesting schedule. See all those RSUs that will be yours every quarter in the future, as long as you stay at the company? All of those RSUs will increase in value if the stock price rises. Even if you sell everything you currently have now, you will still benefit from future stock price increases.

Airbnb Has Already Seen Tremendous Growth. Can You Expect That to Continue?

I subscribe to the thinking that, if you’ve already experienced tremendous growth in a company stock (as Airbnb has over the last 10 years), you shouldn’t expect it to continue. You’ve won. Quit playing the game.

If you think about the basic math of it: it’s easier for a small/cheap company to grow fast than a big/expensive company.

- Take a company whose stock is worth $10. Now 10x it. The stock price grows from $10 to $100: $90 in growth.

- Take a company whose stock is already worth $100. How much growth in the stock does it take to 10x it? The stock price would have to grow from $100 to $1000: $900 in growth. That’s way more than $90 in growth.

(And FWIW, $100 happens to be the last-reported purchase price I heard from a secondary-market transaction for Airbnb shares).

For a bigger, more expensive company, getting 10x growth is a way bigger lift in absolute terms.

(And yes, if you hold Amazon stock, don’t @ me. It is crazy, I know. But one data point does not a strong argument make.)

What I’m saying is, you might think to yourself, “Wow, I can’t believe how much this stock has grown in value while Airbnb was private. I’m going to count my blessings, thank my lucky stars, and take my winnings home with me now.” Wouldn’t be an unreasonable perspective to have. Just sayin’.

If You Also Have Options and Existing Shares

When you have not only RSUs but also options and/or outright shares of Airbnb, you get to be even tax smarter-er.

Let’s say that, as part of your overall strategy for Airbnb stock, you decide you want to sell some (please, say it’s true). You’re then looking at your vested RSUs, your unexercised options, and your existing Airbnb stock wondering, “Well, which should I sell?”

You should likely sell your RSUs first. Why? Because they’ll, again likely, be the shares you can sell with the smallest tax hit.

- Vested RSUs: You will have only held them for a short amount of time, not much time for the stock to change in value.

- Exercisable Options: The very optionality of options is of tremendous value. You’ll probably want to hang on to that. And even aside from that, if your strike price is low (which it would be, if you’ve had these options for several years), then exercising them would likely trigger a bunch of taxes on the big “spread” between exercise price and Airbnb stock price.

- Existing shares: If you have shares from exercising options years ago, you probably have a big gain there that would generate a lot of taxes if sold.

As I mentioned in my post about donating Airbnb wealth to charity:

If you want to donate Airbnb to charity, do not donate your vested RSUs.

There is no tax advantage in the first year of holding the vested RSUs. There is an advantage only if you happen to hold the RSUs for at least a year, and there’s growth during that year. But that could be said of any investment. For Airbnb stock, donate shares you’ve already held for over a year and that already have lots of gain.

Get Yourself a CPA with Experience in IPOs and RSUs

I’m probably just going to copy and paste this section into every blog post I write about this IPO from here on out. Because the taxes can get bonkers. And they can bite you. And you do not want to arrive at April 15 of 2020 (or 2021) and be all, “What is this 5- (6-?) digit tax bill? And why is my underpayment penalty so big?”

The short of it is: The day the RSUs vest, they are considered taxable income. Airbnb will likely withhold the usual, statutory 22% of your RSU shares in order to cover tax. Your marginal (top) tax rate is likely already well over 22%…but factor in $100ks of additional RSU income, and it sure as heck will be. If you owe 35% to the IRS, and Airbnb withholds only 22%…well, I hope you can see the problem.

A CPA can help you figure out both how much tax you owe on your RSUs and when you need to pay it. (I see estimated tax payments in your future.)

If, by some miracle, Airbnb allows you to automatically withhold more than 22% upon vesting, I highly encourage you to do that.

Talk with Someone

I know this is a lot!

With my clients, the eventual strategy is not just a result of walking through some objective algorithm. Yes, it involves numerical projections and spreadsheets, but also conversations. Going back and forth. Revisiting it a few times. All to arrive at something you feel good about.

In fact, it took me a long time and many revisions to even write this blog post because this is simply a big, sticky issue with lots of variables. It’s not a straight line.

So, if you’re not working with a financial planner yet, well, sure, either find one to work with, or just start having those conversations with friends. Focus on the why, the “what’s important to you?” Give yourself time and space and emotion to work through that conversation first.

Good luck!

Other posts in this “Airbnb is going public” series:

1. Airbnb Is Going Public. Time to Create a (Flexible) Strategy.

2. Airbnb Is Going Public. What a Good Time to Give Away Your Money.

Do you want someone to guide you through Airbnb going public? Reach out to me at or schedule a free consultation.

Sign up for Flow’s weekly-ish blog email to stay on top of my blog posts and videos.

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Meg Bartelt, and all rights are reserved. Read the full Disclaimer.