This is the story of how I filed my 14-year-old daughter’s taxes, and then opened, funded, and invested a Roth IRA for her, for tax year 2023. Piecing this process together for the first time was a bit frustrating (even for a financial planner!) so I hope you can follow along with a bit more ease.

You should note that I’m not a tax professional. I did my best to ask tax professionals for the right way to do this. (You would not believe how argumentative those folks can be! At least, on Twitter ?.) Turns out, taxes aren’t just a bunch of objective rules. Lots of subjectivity involved!

I’m going to pretend, for the sake of simplicity, that my daughter Alice has an Adjusted Gross Income (a line near the bottom of the first page of the 1040 tax return) of $1000 for 2023, which means she can contribute $1000 to her Roth IRA for 2023. That’s not the same as making $1000…but close.

Why Would You Even Do That?*

Maybe it’s obvious to you, but just in case you’re all “But she’s fourteen. Normal people don’t do this,” let me explain my reasons for doing this.

The “Roth” Means No Income Taxes. Ever.

If your child earned under $13,850 (the standard deduction for a single tax filer in 2023), they will owe no federal income taxes. (They will owe FICA, i.e., Social Security and Medicaid taxes. And you’d want to investigate your own state’s rules, though I’m guessing your kid won’t owe income taxes on low amounts of income.)

Alice earned far less than $13,850 in 2023 and so doesn’t owe any income taxes. She does owe roughly $150 in FICA taxes (half as an employee, half as an employer, as she was, technically speaking, self-employed).

Usually the money you contribute to a Roth IRA is money you’ve already paid taxes on. But because all of her income is not subject to (federal) income tax:

- The money can go in income-tax free (at least at the federal level, and possibly at the state level).

- After we invest it, it can grow tax-free.

- Eventually if will be withdrawn tax-free.

That’s why Roth accounts are so great for kids.

* Every time I write that sentence, I can’t help but chortle. Last school year, my husband was driving my daughter and her friend home from middle school. The girls had attended sex ed that day, in which they’d learned about different, ahhh, acts that consenting adults can engage in. The friend brought up one of the less-vanilla acts and exclaimed, in outrage, disgust, and disbelief, “Why would you even do that?!” This has become, naturally, a catchphrase in my home.

Compounding over That Many Years Is Crazy Powerful.

Perhaps you’ve heard about how you should invest early because the earlier you invest, the easier it’ll be to build wealth. Compound growth for the win! Well, 14 is pretty damn early.

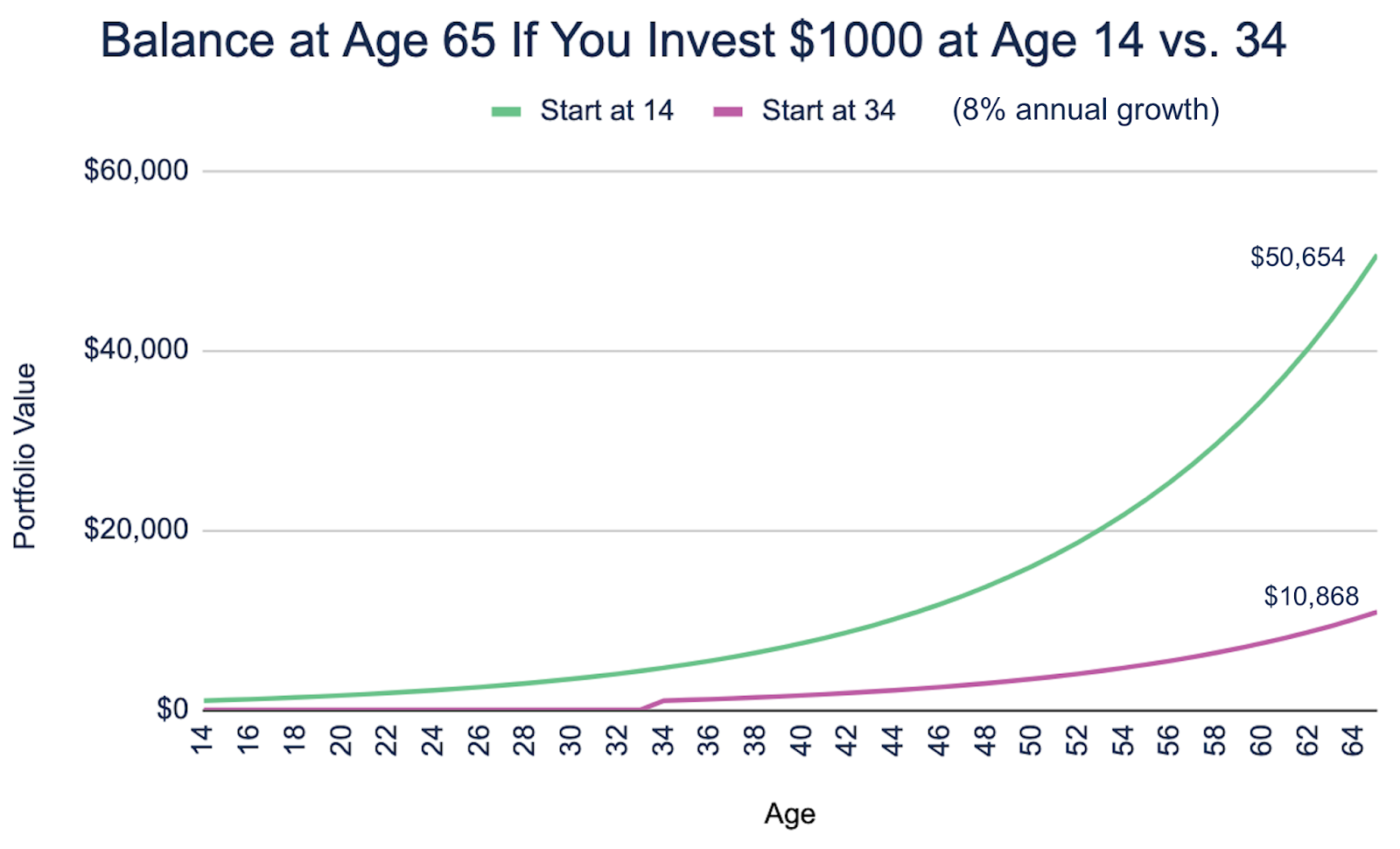

Here’s a simple illustration of the impact. My daughter invests $1000 in her Roth IRA at age 14. In an alternate universe, she doesn’t start investing that $1000 until she is 34 (twenty years later, but still pretty early by many people’s standards for retirement savings!).

By age 65 (the stereotypical retirement age), you can see how much more that $1000 has grown (assuming 8% average annual growth), given 20 more years of compounding: $50,654 vs $10,868.

You Start Showing Your Kid at a Really Young Age How to Do “All This.”

While that ending value (“Fifty Thousand Dollars!”) is fun and all—more so for my daughter than me (“Do you know how much retirement can cost?!”)—I don’t care as much about that.

What I care more about is that I’m starting to show my daughter how to participate in this economy, and that I’m helping her to create the habit of saving and investing for the long-term.

I’m very much hoping that this means that, when she “launches” (my little girl! How can you be leaving the house in just over four years!), at least this part of adult life will come pretty naturally to her.

Oh taxes? Yep, that’s a thing I just do. I remember how maaaaaad mom used to get at how hard it was to navigate that system. Ahhh, good times.

Oh, income? Yeah, I save a good portion of that.

Oh, savings? Yeah, I have a Roth IRA already for that, and I’ll just keep putting the money into stocks via a low-cost fund.

Does Your Kid Need to Have a “Job” Job? Or Could They Just Earn Money Babysitting?

Your kid can just earn babysitting money! Or lawn-mowing money! Or, as my daughter did once, spider-sitting money! (Yes, really.)

The key is documenting the income.

If your kid has a “job” job, it’s obvious. Your kid got paychecks from the employer. If it was a W-2 job, income taxes and FICA taxes will already have been withheld. Your kid will receive the W-2 tax form from the employer after the end of the year. Much like happens for you and your job.

If it wasn’t a W-2 job, then you’re in self-employment territory. The key here is to document your kid’s income. If your kid worked for a company and received a 1099 from them, great! There’s your documentation.

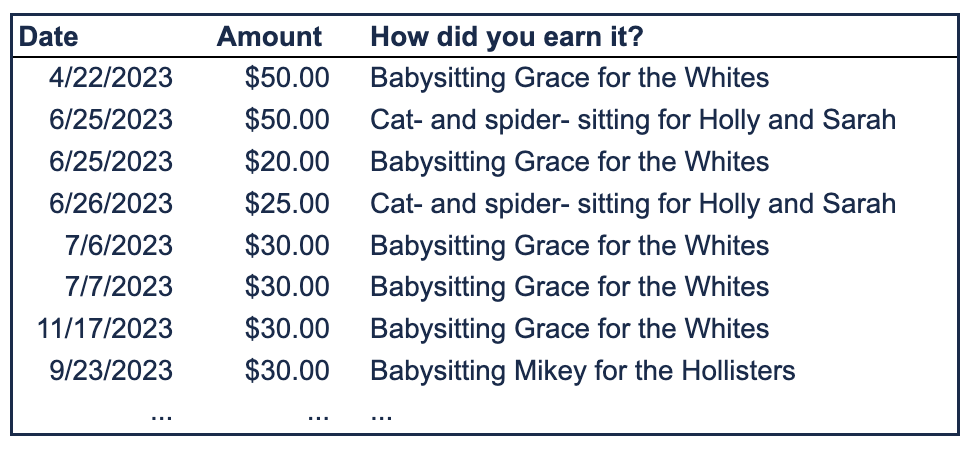

If it’s just from babysitting and spider-sitting for various families, then you need to keep track of the income yourself. This was the case for us. Here’s how we chose to do it.

I have a spreadsheet in my Google Drive entitled “Alice’s Earned Income,” with a tab for each year. And then every time she earns money, I record the date, the amount earned, and what the work was and for whom:

You Have to File Their Taxes. Maybe?

Plenty of tax professionals on Twitter asked “Why would you file taxes for her?” But others reaffirmed my understanding that, if my daughter wants to make an IRA contribution, I have to document her income via a tax return. I honestly still don’t know which is the right answer, because I don’t know which set of CPAs to believe. I went the “better safe than sorry” route and filed her taxes.

After several false starts (and skyrocketing stress levels), I successfully and mostly happily followed the suggestion to use freetaxusa.com, which allows you to prepare your federal tax return for free. State returns cost money. (But ha ha! I foxed them! We live in Washington, which doesn’t have a state income tax!)

Because this was my daughter’s first time filing a tax return, and also because she was under 16, we had to print and mail the tax return, along with a paper check. That was irritating but not too onerous. Hopefully next year we can do at least the payment digitally because she’ll be in the IRS system?

If you work with a tax professional, you could consider asking them to do it. I do work with a good CPA firm, but I wanted to do this myself so as to involve my daughter.

The Biggest Tax Gotcha…for Parents!

One thing most tax professionals warned me about is that

you have to indicate on the kid’s tax return that they are a dependent of someone else.

(You, it turns out.) If you don’t do this, your tax return will be rejected (or whatever the right term is), because you’re claiming your kid as a dependent…and yet they’re saying they’re not a dependent. This, not surprisingly, creates a stupidly large headache for you and/or your tax preparer.

Also, if you have a tax professional prepare your taxes, be sure to tell them what you’re doing.

Open, Fund, and Invest the Roth IRA.

I opened a “custodial” Roth IRA for my daughter. She’s not 18 yet and therefore can’t own her own accounts.

I opened it at Fidelity. Although most of my investments are at Vanguard, they remain there only because of inertia and fear of what administrative catastrophe I’ll bring on myself if I try to move them. (Vanguard’s customer experience has been atrocious for years.) I’ve been a financial planner long enough to know that financial bureaucracy is punishing.

I find Fidelity’s customer experience to be about the best there is out there for consumers, of the established players. (I only use financial organizations that have been around for a while and are stable. Why? I got burned by trying to use a start-up-y fintech tool a few years ago. Behold that sweet UX! It was easy! And free! Then they madly pivoted pivoted pivoted…pivoted right away from the reason I was using them.)

I moved the money in, and, with her blessing, invested it in VTI (Vanguard’s Total US Stock Market Index fund). (Do not consider this a recommendation that you invest in VTI.)

You Can “Match” Their Contributions.

To put the personal finance-nerd icing on the personal finance-nerd cake, the final thing you can do is match your child’s Roth IRA contributions. Of the $1000 Alice puts into her Roth IRA, we, her loving parents, will contribute $500 of that. Money is, as she loves to say, fungible, after all. All that $1000 doesn’t have to be her money.

I have a close family friend (hi, Taylor!) who does the matching for his granddaughter. So, maybe this is something that a finance-nerd grandparent or other loved one of yours can get in on.

To be clear: This match is a legal fiction. It doesn’t enable you to put more money in your kid’s Roth IRA than they’re eligible to. It just means that, of the say, $1000 they earned and are eligible to contribute, you are putting in some of that money. They get to keep $500 to do…whatever. Because, you know, you’re strict but not cruel.

In closing, my daughter was pleased to know that she was being featured in a blog post, but insisted that there is a price to use her name and story. So, here goes: Yes, Alice, I do love you more than your sister.

Do you want to help your child build good financial habits and a solid financial foundation as an adult? Reach out and schedule a free consultation or send us an email.

Sign up for Flow’s twice-monthly blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.