Good on you for wanting to share some of your good fortune, for wanting to help people, communities, and causes that deserve it.

Let’s assume you’ve already figured out the “why” of your giving. And you’ve even figured out the “how much.” (Which are Steps 1 and 2, in our opinion, of the philanthropy conversation.)

Now we’re down to the tactics of giving (the third and last step). This is where many people start the conversation. “I want to give to charity. How about a DAF?” It shouldn’t be.

But for the purposes of this blog post, we’ll assume you’ve done the Much More Important work of figuring out the causes you want to support and the amount of money you want to give away.

Let me give you a wee spoiler: Donor Advised Funds are often not the best way to give away money to charities. Yes, they are very popular in the tech community. Sexy, even. And maybe I’m a contrarian or fuddy duddy at heart, but this makes me even more adamant about explaining all the ways in which they can not be your best choice when giving away money.

How Does a Donor Advised Fund Work?

In a nutshell, here’s how a DAF works:

Step 1: Open up the Donor Advised Fund account with a charitable foundation, for example, Fidelity Charitable, Vanguard Charitable, American Endowment Foundation.

Step 2: “Fund” it, i.e., move money (either cash or investments) into it. There is usually a minimum amount you must commit to putting and keeping in your DAF. This can be from $5k to $25k in the charitable foundations I’m familiar with.

Step 3: Invest it, or leave it as cash. At the very least, you’ll need to sell donated investments for cash in order to donate to charities.

Step 4: Request that the DAF “grant” cash from the DAF to your chosen charity/ies.

There are some important nuances beyond those basic steps that you might not realize. And you really need to if you’re going to use a DAF. Let’s get to those.

The entity that administers your DAF is a charity itself.

When you give money to the DAF, you get all the tax benefits right then and there, because you’re donating to a charity.

You can donate cash or investments. Usually those “investments” are basic stocks, mutual funds, or ETFs. They can also include more-arcane investments, but I don’t know much about that.

One interesting (to me) aspect of it being a charity, is that if you set up a DAF with one institution (say, Fidelity Charitable), you can move that money to another DAF at another institution (say, the American Endowment Foundation) with no tax impact. Why? Because it’s just one charity giving money to another charity.

The useful implication of this is that, if you set up a DAF and find out that you don’t like how it operates, for one reason or another, you aren’t stuck. Sure, it’ll likely be an administrative hassle, because no one likes to let money go, but you can effectively transfer it to another institution.

The Money Is No Longer Yours.

Note that the money is no longer yours as soon as you donate it to the DAF. It belongs to the charity that administers the DAF. You are the “donor” in “Donor Advised Fund.”

You can advise on what happens to the money, like how it’s invested and how much money to give to which charities. That’s why it’s called a Donor Advised Fund.

But you don’t control or own the money any more. If the DAF administrator doesn’t like your idea, they don’t have to honor it.

In practice, as long as your advice is “normal,” for example, you want to give to a regular ol’ 501(c)3 charity, the DAF administrator should do what you want.

It’s an Investment Account.

You can invest the money within the DAF, so it has a chance to grow. Remember, the DAF owner has ultimate authority over how it is invested.

If it grows, you simply have more money to grant to charities.

If it loses value, you have less money to grant to charities.

Neither outcome affects your taxes at all. Why? Because this isn’t your money anymore.

When DAFs are a Good Choice

Before I start poo-pooing DAFs, let’s review the circumstances in which I think DAFs can be a great solution for your charitable urges.

You want to donate securities (stock, funds, etc.), but your chosen charities don’t accept them.

Let’s start by defining a term of art: “appreciated securities.” This refers to an investment (ETF, stock, mutual fund, and other “securities”) that has gained in value (i.e., “appreciated”) since you bought it. “Bought” includes exercising an option and having an RSU vest.

In your case, that appreciated security is likely to be company stock. But it doesn’t have to be. It can be any investment that has grown in value. In the context of charitable donations, you always want to own that security for over 1 year in order to get the tax goodies.

If you’ve been investing (and holding) in the last 10 years in a taxable account (i.e., outside your 401(k)), you likely have appreciated securities in that taxable account. I can say that simply because the stock market has generally increased in value in the last 10 years (recent yuckiness notwithstanding), so most investments have appreciated.

How does this apply to charitable giving?

Because donating appreciated securities gives you better tax benefits than donating cash. You get to:

- Deduct the dollar value of the securities donated (just as you would with cash) and

- Avoid the capital gains tax you’d have to pay on the securities were you to sell them (irrelevant with cash)

Some charities accept appreciated securities. Alas, some do not. Mostly it’s smaller charities that don’t.

So, if you want to give to a charity that doesn’t accept appreciated securities, but for tax purposes you want to donate those instead of cash, then you can:

- Donate appreciated securities to a DAF

- Sell them within the DAF (no tax effect within the DAF!)

- Grant cash from the DAF to charity.

Voilà! Done! Aren’t you clever.

You want to give a bunch of money in one year, for tax purposes, but you don’t want to distribute it to charities just yet.

Maybe your company went IPO this year, or you participated in a tender offer, or something else happened that means your income and therefore tax rate are really high this year. That makes it an ideal year, from a tax perspective, to donate to charity!

Why? Because if your tax rate is 37%, then for every $100 you donate to charity, you save $37 in taxes. But if your tax rate is only 22%, then you save only $22.

So, you want to give away a lot of money this year, to take advantage of your unusually high tax rate. But you don’t actually know which charities you want to give to. You want more time to figure that out. (Good on you! It’s important to take time figuring this out. Philanthropy is a learned skill.)

How do you honor both things?

- Donate all the money to a DAF this year.

- Get the full tax benefit this year.

- Figure out which charities to give how much money to “in the fullness of time.”

- Grant money to those charities from the DAF in future years. There is no tax effect from these grants.

You want to donate appreciated securities to multiple charities

Donating appreciated securities is kind of a hassle. It can be surprisingly administratively onerous, involving paperwork and follow-up phone calls. But so it is.

So, if you donate securities to one charity, you’ll have [this much] administrative hassle. If you donate securities to 10 charities, you’ll have 10x [this much] administrative hassle.

But wait! If you donate securities to a DAF, you’ll have [this much] administrative hassle, and then you can distribute cash (and alllll charities love cash) easy peasy from the DAF to as many charities as you want.

You want to cultivate a family approach to philanthropy.

If you stockpile a bunch of money in your DAF, it might make it easier to involve your whole family, especially your kids and eventually grandkids? (crazy, I know), in crafting a family philosophy around philanthropy.

A DAF that can support multiple years—maybe an entire lifetime—of charitable giving can create a “bigger,” more permanent and organized sense of philanthropy than just your one-off contributions to a charitable cause du jour or your friend’s charitable fundraiser.

I’m personally not sure how persuasive this argument is, as you can still have these conversations with your kids even if you don’t use a DAF. If you approach your charitable donations on an annual basis, each year you can talk with your kids about how much money you’ll donate to charity, which charities you’re donating to, and the why of it all.

When You Should Skip DAFs

There are just as many reasons to avoid DAFs, to just give the damn money to the charity and be done with it. Boring, I know. “Keep it Simple” is possibly Rule #1 of Personal Finance, and it definitely applies here.

Your chosen causes aren’t 501(c)3 charities.

The money in a DAF can only go to 501(c)3 charities. That’s just a special kind of charity as defined by the tax code. Most of the charities you think of are 501(c)3 charities, so this isn’t a huge hurdle.

But it does mean you need to figure out before donating to a DAF that your chosen charities are 501(c)3 charities, i.e., whether your donations will be tax-deductible. (I will specifically call out, because the nomenclature is confusing, that 501(c)4 charities cannot receive money from a DAF.)

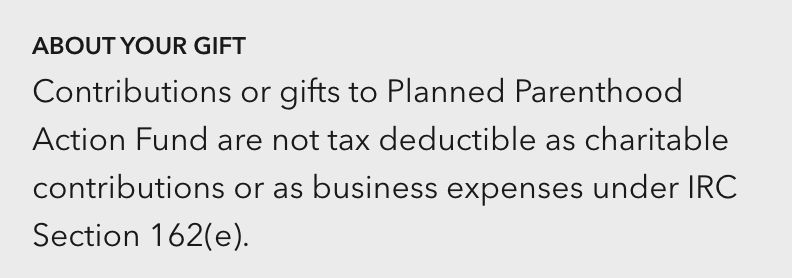

You should be able to find this information on your charity’s website, maybe even right at the bottom of the home page. For example, you can find this at the bottom of the Planned Parenthood Action Fund’s website:

Other examples of charities that many of our clients care about but that are not 501(c)3 charities?

- The ACLU

- The Sierra Club

- All political campaigns

You can easily give directly to the charities.

As I mentioned above, donating appreciated securities to a charity is a pain. But if you’re going to donate securities to only one or two charities, or if you’re going to give cash to however many, then it’s probably easier to just donate directly to the charities and not set up a DAF as a “middle man.”

You don’t want the administrative burden and cost of a DAF.

DAFs are an extra administrative layer in your life. They are an investment account that you have to figure out how to invest. They are another website you have to have credentials for. They’re another interface you have to figure out how to navigate.

In a world where the administrative burden seems to be consuming more and more of our life, do you want to voluntarily add more of it?

Also, DAFs cost money. At Flow, we don’t charge a fee to manage the money in the DAF. (Many financial advisors do; and I think that’s entirely legitimate.) But the charitable foundation that owns the DAF does charge a fee.

So, if you put in cash, and let it sit there, you could be losing 1% of its value every year just to the entity that owns/administers the DAF, not to mention the fee your financial planner might charge.

Paying a fee isn’t necessarily a bad thing. And, as a pro-DAF colleague pointed out: you are not paying the cost. Your DAF is. If you’re getting value for the fee, great! But do be aware that a DAF’s fees will eat into the amount of money you have available to give to charity.

Learn about DAFs Before You Absolutely Need To

DAFs can be powerful tools in some cases. I hope you will take some time to understand how DAFs work before you open one up and fund it. They have some drawbacks, and maybe you’d do well to avoid them.

In particular, if you see a windfall coming up in your future (IPO?), take some time now to investigate DAFs and to think about your charitable giving desires in general. An IPO year will likely be a great year tax-wise to donate to charity, but I don’t want you trying to figure out your charitable intentions and tactics (like a DAF) at the same time that you’re also navigating the frenzied crush of IPO-related decisions and tax-year deadlines.

Thank you for sharing some of your good fortune with others.

Do you want to work with a financial planner who can help you figure out the why, how much, and how of charitable giving? Reach out and schedule a free consultation or send us an email.

Sign up for Flow’s weekly-ish blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.