Are you afraid of the AI bubble? That it’s going to burst and devastate your investment portfolio?

Many clients are expressing this same concern. Here’s what they say (with some poetic license):

AI has dramatically driven up the stock price of all the big tech companies. But there’s no there there in those companies. At least, there’s not enough there there. It’s a bubble. At some point, people are going to realize that Nvidia isn’t worth infinity dollars, the bubble will burst, and all those big tech companies will lose a lot of value and any money I have invested in those companies will go <poof!>. And I will be sad. Very sad indeed.

I know market timing is bad, but still, should we be timing the market?

I can’t knowledgeably comment on all the potential damage caused by the proliferation of AI (though, Lord knows, the abuse of the em dash is damage enough!). But I can usefully comment on how to manage the risk of AI in your investment portfolio.

Market Timing Baaaad. You Know This.

Bubbles are definitely a thing. When they burst, it’s horrible. (Hello, those of us old enough to have lived through the Dot Com Bust, especially if we worked in the tech industry at the time and saw all sorts of paper millionaires become paper un-millionaires overnight.) If you could get out of the market right before the bubble burst, that’d be awesome.

But you almost certainly can’t. There are two problems with trying to get out of the market because you’re afraid of a bubble:

- If you get out of the market too soon, you risk missing big gains.

- Even if you get out at a good time, you risk missing big gains because you don’t get back in at a good time.

There is ample evidence that trying to time the market—in any way—puts you at a severe disadvantage in achieving long-term returns. Yes, the AI bubble might burst in six months…but also some of the best gains ever might occur in the next five.

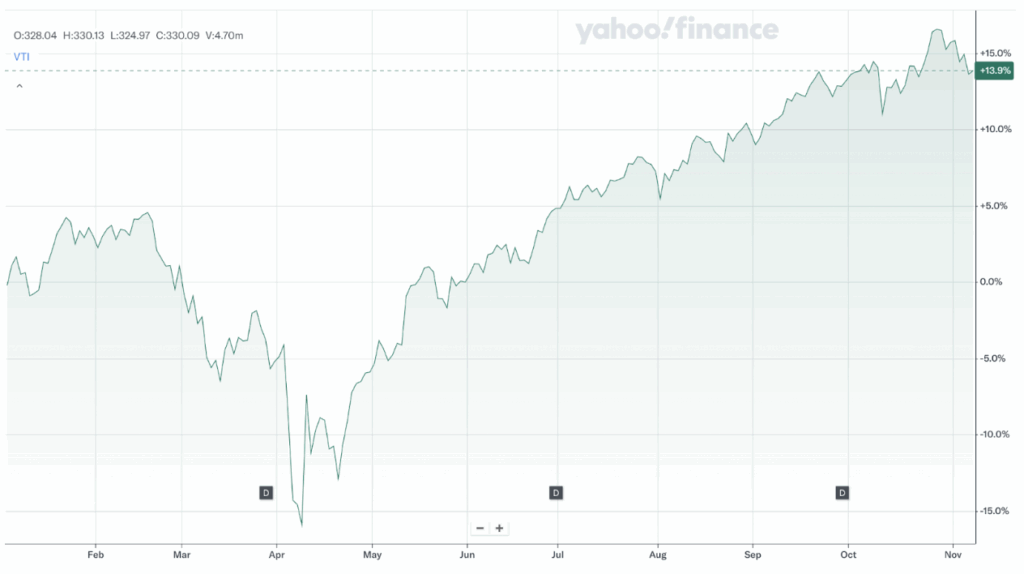

Imagine getting out of the market earlier this year because of fears of Trump or tariffs or the AI bubble. Look at how the US stock market has performed this year (using the Vanguard Total US Stock Market ETF, ticker VTI, as a proxy for the whole market). It’s up 13.9% as of November 9, 2025. Especially look at how it has performed after the tariffs-induced crash in April. Holy rebound, Batman!

Let’s say you are that statistical anomaly that successfully got out of the market at a good time, back in January, because Trump! (Trust me, I feel you.) In April you were feeling pretty darn vindicated. But if you haven’t yet gotten back in because Still Trump! or because of the AI bubble…oh my goodness, you would have missed a lot of growth!

So, if market timing isn’t the answer, what’s a gal to do?

First, let’s revisit some important rules for investing.

What Makes for Good Investing?

While there is boundless commentary on “how to invest” (some of it even useful), I think most people will agree that there’s a short, simple list for the basics of good investing. Let’s discuss some of those here.

For more discussion, read about our investment beliefs here at Flow.

Know when you need your money.

Do you want to buy a house or retire in five years? Or is it in 20? You’re going to invest your money differently depending on the answer.

Why? Because if you invest in the stock market, your investments could lose half their value within one year and not recover the value by that five-year deadline, and you would therefore be unable to meet your goal of home ownership or retirement.

But if you have twenty years to wait before you need that money, you have more time to recover from stock market losses, including an AI bubble burst. Additionally, if you don’t invest in the stock market for a goal 20 years from now, your money will likely not grow enough to be able to buy or retire in 20 years.

Be it too aggressive for a short timeframe or too conservative for a long timeframe, if you invest inappropriately for your timeframe, you risk not having the money you need when you need it.

Know how flexible your goal is.

“Sure it’d be cool to fly first class for that big trip around the world after the kids are old enough to appreciate it, but if we have to fly coach or cut the trip short by a week, I’m okay with that.”

Or

“It’d be the bee’s knees to retire in five years, but I also still quite like my job, so if I have to work another 10 instead, that’d be okay.”

If you can talk about your goals in this flexible sort of way—you’re willing to adjust their price tag or their timing—you can be a little less strict in how you invest for them.

I encourage this framework when it comes to managing a big pile of company stock. If you have a lot of your wealth wrapped up in company stock, it can be very hard to know if you should sell any of it. Even if you know it’s too risky to keep all the stock you have, the lack of a logical strategy for selling it prevents you from doing anything.

Here’s what I usually propose:

- Identify the essential goals in your life. Putting your kids through college. That kitchen remodel. Down payment on a home. Full financial independence at age 55.

- Tally up how much money you need to fund all those goals.

- Sell enough company stock to set aside for those goals (after paying taxes!).

- If you have company stock left over after that, then you can be much more flexible about selling vs. holding the stock. You don’t need the money for anything essential, so you can afford to take more risk (by keeping a concentration in this single stock) if you want.

The same logic applies to investing in general: if you have goals that are “nice to have”—not “must have”—I believe you can be more loosey goosey with how you invest for them.

Yes, I still think that statistics work the same no matter your goal, i.e., a diversified portfolio with a balance of stocks and bonds appropriate for the timeframe is the most likely way to grow your money. But if you’re okay with the possibility of not having enough money at the end of the timeframe, you can reasonably choose to invest far more conservatively (you’re less likely to lose as much, but nor will it grow as much) or far more aggressively (maybe it’ll go to the moon! But also maybe it’ll plummet to earth).

Diversify.

Diversification—making sure you own a bit of every kind of investment asset—is the “magic” solution to managing risk in any single company, sector, country, etc.

Do you work at Chime and 90% of your net worth is in Chime stock because the company just went public and all the RSUs you’ve acquired over the last four years just vested? Diversification will reduce your risk.

Is all your money in US stocks, no international stocks or bonds? Diversification will reduce your risk.

More to the point of this blog post: Is all your money invested in the S&P 500 (which is dominated by Big Tech/AI companies) or, more risky, the Nasdaq 100 (even more so) or, more risky still, just a handful of Big Tech/AI stocks?

Yeah…you’re in for a very bumpy ride if/when the AI bubble pops. Aaaaand diversification will reduce your risk.

If, on top of Big Tech/AI stocks, you also own:

- the rest of the US stock market

- international stocks

- maybe even some bonds (whuuut?!)

then all that is money that likely won’t be so devastated by the bursting of the AI bubble.

Write down your strategy.

Let’s say you have a lot of Bitcoin or Google stock. You constantly worry that “something” should be done, but you can’t bring yourself to actually do anything. One of the biggest causes of your paralysis now is that you had no strategy when you acquired it.

As you were acquiring Google stock or Bitcoin, you could have created a reasonable strategy like “If Google stock exceeds 20% of my total investment portfolio, I will sell the excess and invest that in my diversified portfolio” or “Every time Bitcoin’s value reaches another $10k high, I’m going to sell half of that increase and invest that in my diversified portfolio.” Make your own rules, but make sure they are clear. Rules that leave no wiggle room or uncertainty.

For more traditional investment portfolios, with their boring mix of index funds and ETFs, your strategy might look something like this:

For my goal of retiring in 20 years, I am going to:

- Invest 90% of my money in stocks and 10% in bonds.

- The stocks are going to be 60% US stocks and 40% international stocks.

- Furthermore, the US stocks are going to be 80% large-cap stocks and 20% small- and mid-cap stocks.

- All investments are going to have expense ratios under 0.20%.

- I am going to check on my portfolio once a year.

You can make your strategy as high-level or as detailed as you want. For example, you could say you are going to invest 90% in stocks and 10% in bonds, or you could say you’re going to invest 3% US small-cap value stocks, 3% US small-cap growth stocks, 3% small-cap blend stocks, and so on through all the various “asset classes.”

The more general the strategy, the easier it is to manage. The less poke-poke-poking you’ll do. The more detailed it is, the more advantage you can possibly get from differences in how each different tiny piece of your portfolio performs. On the downside, you’ll be tweaking your portfolio far more often. And as Warren Buffet purportedly said, “Money is like a bar of soap. The more you touch it, the less you’ll have.”

If you don’t have a strategy, how will you ever know that you have too little or too much of something, and what to do if you do identify a deficit or surplus?

Protect Your Portfolio from the AI Bubble.

What does all this “investing best practices” stuff mean for what you should actually do to protect yourself?

In a word: Rebalance.

In many more words that might actually mean something to you:

Start by ensuring you have a strategy for each life goal. If you don’t have a strategy already, create one. If you are feeling emotional about it (which you probably are, and emotion is the killer of prudent investing), I recommend you hash it out with someone else you trust to be knowledgeable and (relatively) impartial. Hey, like a financial planner!

If you already have a strategy, then I encourage you to review it. Does it still make sense for your goals, both the timeframe and the flexibility?

Then at least every year, and possibly even after major market movement, look at how your actual investment portfolio matches up against your strategy. If it differs significantly, then you need to buy and sell to bring it back in balance. Hence the term “rebalance.”

Is your Google stock worth 30% of your portfolio now? You know you need to sell that 10% excess.

Is your portfolio 60% in the S&P 500 (a Big Tech/AI-heavy index) but your strategy said it should be only 45%? You know you need to sell that 15% excess.

If you have new cash to invest, you might not need to sell anything that there’s too much of. You can use the cash to buy more of what you have too little of. This makes sure that the balance or ratios between all your investments are as prescribed.

If you’ve been invested in the US stock market and haven’t rebalanced recently, you likely are overweight Big Tech/AI companies, simply because they have grown so much in the last year or so. This, in turn, probably means you need to sell some of your Big Tech/big US company stock investments, be it individual stocks or funds that are dominated by those companies.

You can then take that money and buy more of other types of investments: smaller companies, international stock, bonds. Oooh, oooh…even better: take a gander at those inflated values and donate the shares to your local food bank! (You can read more about this strategy in this write-up of how I created my own charitable giving strategy.)

In a way, it really is That Simple.

- Create a strategy. At a high level, this dictates how much of each kind of asset you are going to own.

- Check if your investments still abide by that strategy.

- If you own “too much” of one asset, sell some.

- If you own “too little” of another asset, buy some.

After you create the strategy (which yes, involves some level of guessing), there is no guesswork here. No market timing. Just prudent, boring, rational ways to manage risks of all sorts along your investing journey. A way to disconnect yourself from all the anxious hand-waving about AI (at least, from an investment perspective).

This does not mean your portfolio won’t suffer if the AI bubble bursts. It does mean you are more likely to weather any investment storm a little better.

Do you want a strategy for your investments that makes sense to you? That you have confidence in?